by Mike Plambeck

Real estate can be a solid investment, but just having a property up for grabs does not guarantee you high-quality tenants. You have to know and understand market demands, and you have to learn how to present your rental property in the most attractive light. Here are some strategies that will help you attract droves of potential renters to your property so you can find the right potential renters.

- High-Quality Photographs and LOTS of Them

Nowadays, if a rental listing does not have photographs attached to it, most people won’t even look at it. In fact, most people automatically filter out listings without photos, which means that several listings are going completely unseen. Do yourself a favor and take tons of great photos of the space (you may even think about hiring a professional photographer) from as many angles as possible – strive for at least 10 pictures. Open all of the blinds for natural light and make sure the interior is spotless. It is also a good idea to include photos of the exterior and neighborhood as well. People lead busy lives and if they can immediately see what your rental offers, there’s a better chance they’ll reach out.

If you want to really step it up, include a video walkthrough of the space, which can capture a home’s layout in a way that photos just can’t.

- Be Detailed

When describing the rental property, include anything and everything that a renter might want to know – as well as details they may not even realize they want to know. Simply listing the number of bedrooms and bathrooms is not enough. You need to mention the stainless steel appliances, hardwood floors, energy-efficient features, fenced yard, and anything else you think might attract the modern renter. If there is anything unique about the unit, such as high ceilings, make mention of it. Listing sites like LiveLovely.com make it easy to highlight the important details, so take your time to make your post impeccable.

- Be Clear on Your Policies

You don’t want to waste anyone’s time or have to field countless inquiries from people who are not a good fit for the rental. For instance, if you will never allow pets of any kind or any size for any reason, you need to be specific and concise in the advertisement; otherwise people will be messaging you simply to ask. Make sure to include as much detail as possible regarding the utilities, deposits, garbage, and gas costs, and any other general rules that a tenant may need to know while making their decision. The most important policy is, of course, rental payments. Let tenants know the penalties for late payments and be sure to enforce them. Tenants appreciate ease, so consider incorporating online rent payment service options for landlords that make it simple for renters to pay—and simple for you to receive your rental income.

- Advertise Everywhere

Once you have your advertisement figured out, with tons of great photos and written content ready to go, you need to actually get the word out there. Choosing to post your rental advertisement in only one or two places is a big mistake. With so many great avenues out there for apartment hunting, people no longer stick to just one source when looking for a new home, which means that you need to avoid sticking to one source too. From the newspaper and grocery store bulletin boards to websites like Craigslist and Zillow, you need to make a list of all the places you can take advantage of and list your rental unit in all of them. And after all that, make sure to also put a sign up in front of the apartment or home (include as many details that will fit), because a lot of people also drive around neighborhoods that they are interested in.

- Respond & Take Note

You may get tons of messages and calls regarding the apartment, but try your best to respond to everyone – even if it is just to let them know that the place has been rented and is now off the market. If someone really loves it, they may be okay with your keeping their information for the future. You never know what may happen with your first renter, so it’s a good idea to have a couple backup tenants in your pocket.

by Mike Plambeck

The FHFA’s (Federal Housing Finance Agency) Home Affordable Refinance Program was scheduled to end next month. September 30th to be exact. Fortunately for many homeowners that isn’t the case anymore. Introducing HARP 2018

The FHFA made an announcement on Thursday that the now HARP 2018 program is being extended through Dec. 31, 2018, which will add an additional 15 months to the program’s already extended lifespan. The now extended program will allow Fannie Mae and Freddie Mac to implement some new streamlined refinance offerings. This will be targeted towards borrowers with high loan-to-value ratios.

Get Help Pre Qualifying for a Low Credit Home Loan – Click Here!

The FHFA said Thursday that the new HARP high-LTV refinance program is going to unveil in October, but the program is still being modified slightly, which makes it necessary to extend the HARP deadline through all of 2018.

The FHFA said in its announcement Thursday that they are going to establish an eligibility date which will make the new refinance program available for loans originated on or after Oct. 1, 2017.

Under the new changes, the government sponsored enterprises (Fannie and Freddie) will “modify the structure of future risk-sharing transactions to accommodate the High Loan-To-Value Streamlined Refinance program by allowing the recently refinanced loans to return to the reference pools in place of loans that prepaid,” the FHFA said. The first rule to eligibility is that your loan must be a conventional loan mortgage backed by Fannie Mae or Freddie Mac

The FHFA says that this change will help preserve credit loss protection on the mortgages without undoing the protection paid for via CRT transactions.

The FHFA also stated that the changes to the HARP 2018 High Loan-To-Value Streamlined Refinance program “will appropriately balance continuing to offer assistance to underwater borrowers with protecting taxpayers.”

The HARP 2018 refinance program is a great way for homeowners that may be upside down or have lost their equity to refinance their mortgage. By doing this it will generally put them back into better financial mortgage shape. This could make all the difference in the world when it comes to ensuring you can make your mortgage payment and avoid possible foreclosure.

Related Articles:

Fannie Mae HomePath Mortgage

HARP Loan Program Guidelines 2017

HUDHomestore and Buying HUD Homes

by Ken Bartz

There are tons of tips out there on how you can improve your chances of getting your mortgage approved. And it’s no surprise, either. Buying or selling a house can be a stressful time, especially for first-time home buyers, and the thought of your mortgage application being rejected is an added stress that you just don’t need.

In the near future, this stress may be reduced, according to an article published by Monster Lead Group discussing how “Machine learning and the resulting AI will make a high-stress and non-consumer-friendly process, like a mortgage, frictionless”, said Alex Kutsishin, chief marketing officer for Sales Boomerang.

But until super smart robots become the norm in the mortgage sector, we still have to deal primarily with human lenders. The key to getting your mortgage approved is understanding loan officers. What is it that they actually look at when assessing a mortgage application? We explore this question in this article to give you the inside scoop on getting your mortgage approved.

Getting Your Mortgage Approved – How To

What do loan officers consider?

It’s not as simple as having a solid credit score and a respectable income (although these are still important factors). Loan officers look at lots of different criteria when considering whether it is worth the risk of approving your loan or mortgage. Here are a few of the key factors.

Debt-to-income ratio

Being in debt can be a black mark on your report card, but it doesn’t automatically disqualify you from getting a mortgage. What’s more important is your debt-to-income ratio (DTI). This considers your total monthly debt payments compared to your gross monthly income.

DTI is calculated by totaling your monthly debt payments and dividing this figure by your gross monthly income, multiplied by 100 to come up with a percentage. This calculation is used to assess whether you are capable of managing all of your monthly payments. A high percentage would be a red flag to lenders while lower percentages are more likely to get you approved.

Loan-to-value ratio

Another ratio for measuring a mortgage lender’s risk is the loan-to-value ratio (LTV). This figure compares the amount of money you are looking to borrow with the total value of the house. Your LTV ratio can change over time, something we’ll come back to later in the article.

For example, if you are borrowing $180,000 for a property valued at $200,000, your LTV will be 90%. The remaining 10% represents the deposit you are putting down on the property. The higher your down payment is, the lower your LTV will be. This means less risk for the lender and better chances that they will approve your mortgage.

A high LTV doesn’t necessary mean you’ll be rejected, but approved mortgages with high LTVs are likely to have higher interest rates.

Too much shopping around for mortgages

It makes sense to shop around for the best rates when looking for a loan or mortgage, but be careful when doing this. When you apply for a loan or request a quote from a lender, they will perform a search on your credit file to check your credit history. These searches are visible on your file, so when you apply for your mortgage, the loan officer will see them.

If you have multiple searches within a short span of time that’s around the same time as your mortgage application, whether they’re from quotes for a mortgage, credit cards, or other loans, this can reflect badly on you. Lots of searches might indicate that you are desperate for a loan, which suggest that you are unable to make the necessary repayments and will make the lenders uneasy and less likely to approve your mortgage. Always try to make sure you have the best possible credit scores to get the best possible mortgage rate.

Some credit card companies offer “soft search” tools that allow you to find out if you are likely to be approved without putting this mark on your credit file. So, if you are in need of credit, look out for these instead.

Employment history

Your current income is a strong indicator of whether or not you’ll be able to make repayments on time, but loan officers will typically look further into your employment history to assess your level of financial stability.

If you’ve been recently fired from a job, unemployed for a period of time, or are constantly jumping from one job to the next, this could raise red flags. Lenders may look at the previous 24 months of your employment history to determine how reliable you will be in terms of future income.

Likelihood of the value of the property going down

The value of a property can fluctuate a lot over the years, and for a variety of reasons. Changes in the state of the economy or the property market can see house prices rise or plummet, renovations made to a property can increase its value, and changes in the local area can have positive or negative effects, there are many factors at play.

If you have a mortgage on a property and the value of the property increases, then your loan-to-value ratio decreases. Any repayments you have already made on your mortgage will decrease the LTV even further. Since a lower LTV means less risk for the lender, they are hoping that the property value will increase.

A decreasing value could see the LTV rise above 100%, meaning the lender is more likely to lose money if you, the property owner, can no longer pay their mortgage payments. So, if an evaluation of the property shows that its value is likely to go down, this will lower your chances of getting approved. If you want to find out how at risk your property is for devaluation, check out these 10 most common things that devalue your house.

To sum up…

Don’t hang all your hopes on getting a perfect credit score, or give up completely just because you owe some debts. There are lots of different factors that contribute to the success of your mortgage application.

Try putting yourself in the shoes of a loan officer reviewing your mortgage application. Would you approve yourself? Think about the things they might pick up on as high-risk factors and work on improving these before you submit your application. Like with most things, preparation and knowing what you’re getting into are extremely valuable if your end goal is getting your mortgage approved to get your dream home.

Related Articles:

Top 5 Things To Know About Getting A Mortgage

How To Compare Mortgage Rates

by Mike Plambeck

Before the last housing bust, it was easy to secure a mortgage loan with bad credit. This has been blamed for much of what blew our economy to smithereens. To avoid the next financial disaster, banks are taking the time to thoroughly check your credit when you apply. There is no need to lose heart, however, if your credit is not perfect. Here are 6 tips to fix your credit when buying a home.

Check Your Credit Scores FREE

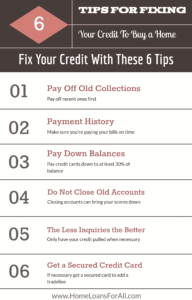

6 Tips To Fix Credit When Buying a Home

Tip 1: Pay off old collections

The first step to fix your credit is to pay off any collections or judgments as quickly as possible. Make sure you then contact those creditors and request that they report those accounts as paid. Lenders make human decisions; so even a judgment that has a few years before it drops off your report will look better if it says paid next to it on your credit report. If paying off collections and other negative items just isn’t financially possible……..mortgage preparation/credit restoration is an excellent option to fix your credit, bring your scores up quickly and have you mortgage loan ready in a very timely manner.

Tip 2: Payment history

Paying bills, especially credit cards and other revolving credit accounts on time and regularly, shows responsibility. That’s what lenders want to see: Not only your ability to pay the loan back, but your willingness to do so. Get those over limit and past due accounts shored up as soon as possible. Then, keep paying all your bills on time, including your utilities. If you go on vacation and your cell phone company hits you with a $1,000 roaming charge, haggle or settle with them; don’t walk away from that bill. It will only continue to haunt you. If your cable company makes you angry by raising your rates or changing your channel package, don’t shoot yourself in the foot by not paying a $200 bill.

Tip 3: Pay down balances

Reduce your credit card balance to 25% or less of your credit limit on every card. On most free credit score websites today, they will show you with color graphics when you are hitting the “red line” on your optimal account debt. Don’t apply for new lines of credit. Nothing dings your credit faster than inquiries from financing companies; especially when you already have high balances. It makes you appear as if you are “fishing” around for money you don’t have or can’t pay back.

Tip 4: Do not close old accounts

Closing your credit card accounts won’t fix the problem. It is only like chasing your tail, because your high open balances then reflect as a higher percentage of your overall credit availability. Consequently, if you have an old credit card that you laid aside early in your plan to improve, break it out and use it in small purchases that you can pay off by the end of every billing cycle. This will show up on your credit report as responsibly handled credit.

Tip 5: Don’t let anyone pull your credit

Don’t make major purchases on credit, even if it is some “90 Days, Same as Cash” mumbo jumbo at the warehouse store. That big screen TV looks nice, but leave it on the shelf in the electronics department. You can wait until you are in your new house to pick up all the goodies to go with it. Don’t listen to the dealer when he tells you it will cost you more to fix your car than it is worth; right after he sees you looking at the latest luxury models on the lot. Take your keys, thank him for the free diagnostic tests, and truck on over to the guy your friend at work knows who charges a third of the price for the same repairs.

Tip 6: Get a secured credit card (if necessary)

Other little things, such as getting a secured credit card, or subscribing to a credit update service, can be helpful; but they aren’t really necessary. Secured credit cards are for people who have fallen completely off the credit radar. If it’s been months since you had an active credit card, all your accounts are in collections, or you have recently come through a bankruptcy; then by all means, use a secured card to get a foothold. If this is the case, however, be prepared for the journey back to functional credit to be a long one. Where there is a will, there is a way. Be patient. Be vigilant.

Conclusion

Remember, a reputable lender will be on your side. They want you to win the credit battle, because they want you to qualify for the loan. It’s how they make their living. So, they will gladly tell you which credit card to pay off soonest if you can’t pay them all. Regularly checking with your lender as you move through the process of credit repair to fix your credit will help speed the process. Feel free to call them if you have any question about any decision regarding your credit…..like the telemarketer on hold trying to sell you a timeshare! Home Loans For All only partners with lenders that will be there for you and more than happy to keep giving you credit advice every step of the way. We hope these tips to fix credit have helped.

by Valerie Kriss

When you take out a mortgage, you’re in it for the long haul – traditional home loans usually take decades to pay off, and a smart home buying budget incorporates mortgage payments and long-term interest into the cost of home ownership.

But what if you could pay off your mortgage early? In this post, we’ll show you a few tips to pay off your mortgage early.

First, let’s look at some reasons to commit to paying off your mortgage ahead of time.

Prepare for retirement

If you’re in a position to pay off your mortgage sooner than planned, you’re probably a diligent saver. You’re already aware that retirement is challenging and often expensive in its own right. Paying off your mortgage early will eliminate one big financial uncertainty – and it’ll protect you from any sharp turns in the housing market. Plus, when you’re debt free, you’ll have the added incentive of knowing that all the money you earn is money you can save for the future.

Pay your kid’s college tuition

You want your budding genius to attend a top-tier school, even if you have to pay top-tier tuition. If you can pay off your mortgage before your children are college-bound, you won’t have to fight a debt war on two fronts. You and your family will have more flexibility when it comes to choosing the right university, and your kids will have more financial security when they graduate.

Decimate your total interest

As with any long-term loan, a significant percentage of your total mortgage cost is a quarter-century or more of interest. This can add up to tens of thousands of dollars over the course of a decade. Think about what you can accomplish by reinvesting that money. If you have an adjustable-rate mortgage, settling your mortgage early will also protect you from interest rate hikes down the road.

Tips To Pay Off Your Mortgage Early

Tip 1: Pay down the principal

If you can scrape together a lump sum, use it to pay down your principal. Most mortgage lenders will allow you to make a payment on the principal alone, rather than the combined principal and interest. Paying down even a small fraction of your principal, especially early on, will save you a significant amount in interest charges down the line – not to mention truncating your total mortgage time. If you don’t have enough money to make a large principal payment, make regular smaller ones. For example, say your monthly mortgage payment is $1332 per month. If you can round up to $1500 or even $1400, those principal payments will add up to hundreds or thousands per year.

Tip 2: Switch to a biweekly payment

Instead of paying once a month, pay fifty percent of your monthly rate every two weeks. In other words, if your usual mortgage payment is $1500 per month, you would pay $750 every other week. This will have a similar impact on your monthly budget, but dividing your payments into weekly rather than monthly installments means that you’ll make a total of thirteen full-size payments per year instead of the usual twelve. You won’t feel like you’re digging deep for the extra funds, but you’ll wind up making an entire extra payment per year – shaving a few years off your total mortgage time-frame.

Tip 3: Refinance for a shorter schedule

Do you have a thirty-year mortgage? Ever thought about refinancing your mortgage? Refinance it as a fifteen-year mortgage. You may score a lower interest rate, and you’ll pay much less in interest overall. In other words, you’ll be making smaller payments for fewer years. If you can’t cut your mortgage period in half, consider a twenty-year loan instead. Even if you don’t officially refinance, you can still cut down your time-frame – simply commit to repaying your mortgage more quickly, and build a monthly budget and schedule around your new numbers. You can use an online mortgage calculator to play around with some numbers.

Tip 4: Commit your windfalls

Most people receive a few windfalls over the course of the year – tax refunds, annual bonuses, gifts. If you can use all or even most of this extra money as an extra payment on your mortgage, you can make significant progress towards cutting down your debt. Each year when you receive a raise, commit to spending a percentage of it on your mortgage – even if it’s just a few hundred additional dollars per year, it’ll add up. This strategy has the advantage of using money you won’t miss – you’re not used to it, and you’ve already learned to budget without it. Using it to reduce your mortgage is one of the best investments you can make.

If you’re a homeowner in a position to radically shorten your mortgage schedule and pay off your mortgage, you’ve already established an impressive record of planning, saving, and budgeting. These few tips to pay off your mortgage can give you an enormous advantage in the mid- to long-term, and they’re easy to seamlessly integrate into your existing financial habits.