by Mike Plambeck

Finding low income housing in Los Angeles can feel like an impossible task. Finding low income housing in Los Angeles for single mothers? Even harder. The home buying process is difficult enough even when you’re not trying to raise a family alone on top of that.

Moreover, many single mothers find themselves having bad credit or low income for reasons that are completely beyond their control. A lack of time to work or outstanding debt from legal fees may mess with homebuying plans.

Don’t you fret! Low-income housing in Los Angeles for single mothers is available and affordable. If you know where to look for it and how to apply for it, you can get your dream home. That’s why we at Home Loans For All have put together this comprehensive resource guide for anyone looking for low-income housing in Los Angeles for single mothers.

We’ll cover the most accessible home loans and where to find the best California home assistance for single moms. By the end of the article, we hope that you’ll have all the information you need to start finding great low income housing.

Get Help Pre Qualifying for a Los Angeles Low Credit Home Loan – Click Here!

Low Income Los Angeles Home Loans

These are what we consider the best mortgages available for anyone looking for low income housing in Los Angeles for single mothers.

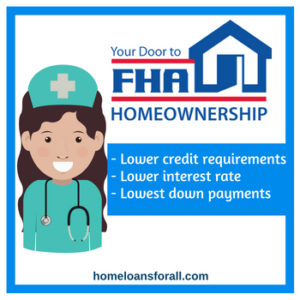

FHA loans for single moms in CA

FHA are there to help because they are interested in your housing as well. You know why? Happy families in their own homes boost the economy!

Most loans either have a low down payment or low credit requirements – not both. Private banks and moneylenders feel that they need to have one or the other to offset the risk of a loan, so the lower your credit score is, the more you’ll have to pay upfront.

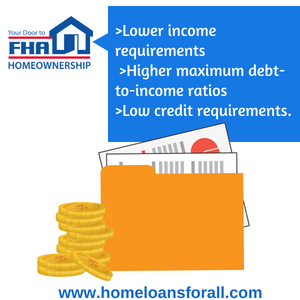

The most commonly-available exception to this rule is the FHA loan program.

FHA loans are, as the name implies, insured by the Federal Housing Administration, an institution backed by the power of the US Treasury.

If you default on your loan because you are unable to make all of the payments, the FHA will pay back a portion of the loan to the lender.

Because this institution is absorbing some of the risks of the loan for the lender, these loans come with expanded eligibility requirements and bring you the “best of both worlds” by combining low minimum credit requirements with inexpensive down payments.

If you have a FICO credit score of 580 or more, you will only have to pay 3.5 percent of the loan upfront. If your credit score is at least 500, the most you will have to pay is a 10 percent down payment.

Combine that with expanded income eligibility requirements, a maximum debt-to-income ratio of 50 percent (instead of the usual 40), and lower interest rates, and you’ve got a home loan program you can’t afford to ignore!

VA and CalVet loans for single moms in CA

You are a mom and a Veteran? *makes a low bow*

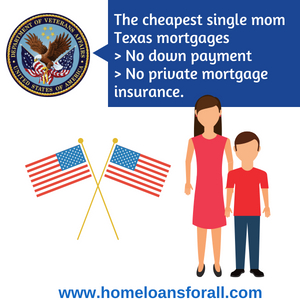

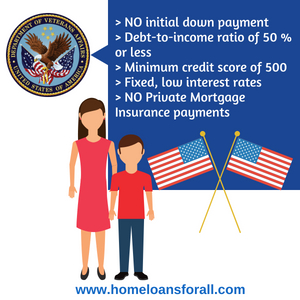

VA loans are also insured by an institution of the federal government – the Department of Veterans’ Affairs, or “VA”. Because of that insurance, VA loans have even more generous eligibility requirements than FHA loans.

They can also save you thousands of dollars because they require no down payment at all and waive the Private Mortgage Insurance requirement on FHA and conventional loans.

CalVet loans are basically the same thing, except that they’re insured by the California VA instead of the federal equivalent.

The biggest practical difference between the two loans is that CalVet home loans for single moms will often have slightly lower interest rates. It is saving you a bit of money over time.

The one downside that both of these programs share is the fact that, because of the nature of the institution insuring them. The only single mothers who will be allowed to apply for these loans will be veterans who have served for at least 181 continuous days of active duty or the widows of a veteran who was killed or went missing in action.

If that describes your situation, consider applying for a VA or CalVet home loan for single mothers in California today.

CalPLUS Home Loans

CalPLUS home loans are mortgages for first-time buyers that are specifically designed for low-income homebuyers in California (you can read more about CalPLUS income limits by county by clicking here.)

These FHA-insured mortgages have higher interest rates than traditional FHA loans, but allow you to cover most or all of the initial down payment with a deferred down payment assistance loan that doesn’t have to be paid off until you’ve finished paying off the entire mortgage.

If you’re not a veteran and your biggest concern as a single mom home buyer in California is making the down payment upfront, this is a great program to consider.

Los Angeles Home Loans For Single Moms

The following are the most common home loans offered to single moms in the city of Los Angeles. Some of these loans come with high credit and income requirements and are not recommended for those looking for low-income housing in Los Angeles for single mothers. However, we still wanted to go over these programs so that you understand all of the options that are available to you.

Conventional Loans for single moms in CA

Conventional loans are the most common form of home loan in the country, but because they’re designed for upper-middle-class customers they are not good choices for many home buyers.

You may find yourself struggling with the conventional loan, whereas there are other, more convenient options.

Conventional loans require minimum credit scores of 660 to 700, require you to pay 20 percent of the total value of the home upfront, and usually have income limits that shut out those looking for low-income housing in Los Angeles for single mothers.

USDA Loans for single moms in CA

US Department of Agriculture Rural Development Loans is a home loan program that we frequently recommend to Los Angeles home buyers, even though it’s not exactly a California low-income home loan. USDA loans have fairly high credit and income requirements – usually a little bit lower than the requirements for a conventional loan and significantly higher than those of an FHA or VA loan.

The benefit of USDA loans is that they give you the option to waive the initial down payment. You can do that and instead pay off the loan entirely in monthly installments.

These installments also have lower interest rates than conventional loans. This means that if you can successfully apply for this type of loan it may save you money in the long run.

California Home Assistance For Single Moms

If you’re having trouble finding a home loan and have explored all of the options above, here are some other things you can do to find low-income housing in Los Angeles for single mothers:

Find A Cosigner

This option is specifically for single mothers in California who have bad credit. Lenders know that sometimes bad credit happens to good people, so they allow you to have someone else co-sign your mortgage as a kind of recommendation that says “This person can be trusted to make their payments.”

The co-signer ties their credit directly to your property, allowing you to apply as though you had a higher credit score than you actually do.

However, they absorb some of the risks and may be expected to make some of the payments if you default on your mortgage or fail to make a monthly payment. This is why co-signers are usually a trusted family member or friend.

Try Renting To Own

Rent to own is a very good option but not that many houses are available. You might not find your dream home!

A rent-to-own contract in California is a standard rental contract that comes with an initial upfront payment. It is a potential options fee – that gives you the option to buy the home in full after the lease has ended.

This is a good option for California single mothers who know that they want to own a home at some point but who aren’t able to afford or apply for a home loan at this time.

The period of time that the lease takes up is a great chance to start saving up for the down payment and doing some credit repair. So, you can get more favorable terms once you’re looking for an actual mortgage.

Down Payment Assistance

Is the initial down payment keeping you from buying the home of your dreams? This is the case for many people looking for low-income housing in Los Angeles for single mothers.

Even if you can afford to make monthly payments, paying thousands of dollars all at once is beyond the abilities of many low-income buyers.

The California Housing Finance Agency has a few down payment assistance programs that can help a low-income home buyer with that initial payment. The CalPLUS loan, which we wrote about in detail above, is one example.

The MyHome Assistance Program is another one that can be combined with any loan of your choosing. It will help you pay up to 3.5 percent of the down payment using a no-interest deferred loan that you don’t have to pay off until the mortgage has ended.

Lenders in your area may offer other forms of down payment assistance. Be sure to ask them about it before applying!

Housing Choice Vouchers

If you have exhausted all other options for finding low-income housing in Los Angeles for single mothers, it may be time to consider public housing. In the state of California, you can find housing choice vouchers (HCVs) by contacting your local Public Housing Authority or one of the six regional offices of HUD in California.

The latter can be reached for assistance and advice by calling (800)955-2232, a number that is available in either English or Spanish.

Low Income Housing in Los Angeles for Single Mothers

We hope that the home loans and resources listed in this article will help you find great low-income housing in Los Angeles for single mothers. We know how hard it can be to find a good home in this city on a budget.

If you find these resources useful and you know someone else who could benefit from them, please consider sending them this article. You will help us get the word out about our site.

by Mike Plambeck

If you’re looking for Ohio home loans for first responders, there are many excellent options available. VA loans, though not available to all first responders, are some of the cheapest around. USDA mortgages offer those outside of the big cities a chance to waive the down payment and get lower interest rates.

FHA loans combine accessibility and affordability by having no credit requirements and low down payments. And then, of course, there’s the Ohio Heroes program designed especially for first responders, police officers, and teachers.

Get Help Pre Qualifying for an Ohio First Responder Home Loan – Click Here!

In this article we will cover all of these programs in detail, as well as other forms of assistance offered by the state and federal government to help first responders in Ohio buy the home of their dreams. We’ll also help you find a home loan with bad credit or low income.

The Ohio Heroes Program For First Responders

The Ohio Heroes program is offered by the Ohio Housing Finance Agency, or OHFA, to citizens of the state of Ohio who are employed in a job that somehow benefits the public at large (see next section.)

If you apply for the Ohio Heroes program, you are applying for a VA, FHA, or conventional mortgage through the OHFA. But the advantage is that no matter what type of loan you get accepted for, you will have a greatly discounted mortgage interest rate (exact rates vary by county) and can choose to have the state pay the down payment for you.

This down payment assistance is “forgiven” after seven years, meaning that as long as you continue to make payments and live in the house for that long you won’t have to pay back the down payment at all.

This can save you thousands of dollars on your initial and ongoing payments on a mortgage, making the Ohio Heroes program one of the best Ohio home loans for first responders in the state.

Who qualifies for Ohio Heroes assistance?

The Ohio Heroes program for first responders is offered to police officers, firefighters, volunteer firefighters, EMTs and paramedics who have a FICO credit score of at least 640, a debt-to-income ratio of no more than 40 percent, and who meet the Ohio Housing Finance Agency’s income requirements in their area.

You can use this tool, provided by the OHFA themselves, to calculate the income requirements for your county in order to see if you’re eligible for the Ohio Heroes program.

Although it’s not particularly relevant to the subject of this article, which is Ohio home loans for first responders, loans from the Ohio Heroes program are also offered to:

Veterans, active duty military members or members of reserve components (including surviving spouses)

Physicians, nurse practitioners, nurses (RN and LPN) and STNAs

Teachers (pre-K through grade 12), administrators and counselors

Also, if you’re looking for home help for Ohio single mothers, you should click here to see what programs are available for those in your situation.

Ohio Heroes Home Loans For First Responders

These are the three types of home loans that you can apply for using the Ohio Heroes program for first responders.

You can also apply for them separately, which will come with the expanded eligibility requirements (lower credit scores, etc.) described in each section below.

Conventional loans

Conventional loans are the most common Ohio home loan for first responders in the state and is the first type of loan eligible for the Ohio Heroes program.

However, these loans are designed for upper-middle-class home buyers and are too inaccessible and too expensive for many Ohio first responders.

Conventional loans require a minimum credit score of 660 to 700 (depending on the lender), a debt-to-income ratio of 40 percent or less, and a down payment of 20 percent of the total value of the home to be made up front.

The credit and down payment requirements in particular are difficult to achieve for many Ohio home buyers – even if you think you can make regular payments without much trouble, paying a thousand dollars all in one go is a big ask to make of anyone.

Fortunately, the next two home loans for first responders have expanded eligibility requirements and much lower down payments.

FHA home loans for first responders

FHA loans are the most popular form of home loan in the state of Ohio, and when you look at the benefits it’s not hard to see why.

Because these loans are partially insured by the federal government, lenders see them as having less risk and will give these loans to applicants who might be rejected outright for a conventional mortgage.

FHA loans still have down payments, but very small ones – only 3.5 percent so long as the applicant has a credit score of 580 or higher.

And since FHA loans technically have no credit requirement imposed on them by the federal government, you’re likely to have your loan application accepted even if you have a lower credit score than that, provided that you can provide alternative forms of credit or are willing to pay a down payment as high as 10 percent of the home’s total value.

In either circumstance, you’re paying much less than the 20 percent down payment required by conventional mortgages, and you’re much more likely to get accepted.

The only real downside of FHA home loans for first responders in Ohio is that you have to make Private Mortgage Insurance payments for the duration of the loan period, as opposed to only for part of it (which is the case with conventional and USDA loans.)

This means that a conventional mortgage may save you a little money in the long run, but only if you already have the money now to make the down payment or receive down payment assistance through the Ohio Heroes program.

VA home loans in Ohio

VA loans are also insured by a branch of the federal government – the Department of Veterans’ Affairs. As you may have guessed, this means that VA loans are only available to current or former members of the armed forces who have served long enough to receive a VA Certificate of Eligibility.

However, if you are eligible for a VA home loan in Ohio (especially through the Ohio Heroes program), you should definitely apply.

These loans have no minimum credit requirements (although lenders often require a credit score of 500 to 580), no PMI payments, and no down payment whatsoever.

When combined with the more lenient debt and income requirements of the FHA loan, these loans are very easy to receive if you’re eligible and will save you thousands of dollars over time. What’s not to love?

USDA Ohio Home Loans For First Responders – Another Option

USDA home loans are not eligible for the Ohio Heroes program. However, we wanted to mention them as a good alternative, particularly for those in rural areas of the state.

These Rural Development Loans are designed to encourage Ohio first responders (and other home buyers) to consider homes outside of the major cities, with about 97% of properties in the state being considered eligible.

USDA loans aren’t quite as accessible as FHA loans, requiring minimum credit scores of 600 and income that must be less than 115 percent of the median income fin your county.

However, a USDA home loan for Ohio first responders can save you a lot of money in the long run.

USDA loans require no down payment in many cases and only a low down payment in all others and usually have some of the lowest interest rates around.

Conclusion

We hope that this article has helped you to better understand the Ohio Heroes program and the other Ohio home loans for first responders that are available.

Whether you have bad credit, low income, or simply can’t afford to pay a large down payment, remember – everyone deserves to live in a beautiful and permanent home of their own.

by Mike Plambeck

Buying a home is a stressful part of anyone’s life. You have to find a property you like, save up for the down payment, get approved for the loan. It’s a lot of work that becomes a lot more work when you’re also balancing a nursing job with everything else.

Unlike other states and their HERO loans, there are no specific home loans for nurses in Michigan. But if you know where to look, there are lots of great programs offered by the state and federal level that can help make homes cheaper, more accessible, or otherwise better for anyone looking for nurse home loans in Michigan.

Get Help Pre Qualifying for Nurse Home Loans Michigan – Click Here!

Today we’ll cover these loan programs in detail. Whether you’re looking for no down payment, low down payment, or simply to find something that’s a little more convenient and affordable than the conventional mortgage option, this guide should help you find all the information you need about the best programs for nurse home loans in Michigan.

No down payment home loans for nurses in Michigan

Unfortunately, it’s hard to find truly no down payment home loans for nurses in Michigan. Down payments are how Michigan mortgage brokers ensure that they’ll make at least a percentage of their money back when they give someone a big loan. A no down payment home loan is simply considered too great a risk for most private banks and moneylenders.

However, there are many government programs where one government agency or another absorbs a certain amount of the risk for the lender by either insuring the loan or paying it out themselves.

These loans (which include the Michigan FHA loans we’ll discuss in the next section) often have lower down payments than their conventional counterparts, and there are two government programs in particular that can be turned into no down payment nurse home loans in Michigan.

VA home loans for nurses in MI

VA loans are insured by the Department of Veterans’ Affairs. This federal department doesn’t actually pay out the mortgage, but they do guarantee a certain amount of the loan in the event that the home buyer fails to make all of their payments on time.

Because this promise is backed by the power of the US Treasury, these loans are seen as a much smaller risk to lenders and they are willing to accept applicants for VA loans who might be rejected outright for other nurse home loans in Michigan.

VA loans have a lot of great benefits if you’re looking for nurse home loans in Michigan. In addition to the lack of a down payment, these include expanded income requirements, no credit requirements, and no PMI payments (private mortgage insurance).

So VA loans aren’t just more attainable, they’re also a good way to save thousands of dollars on your home.

The one downside of VA loans is that they’re only available to veterans and eligible service members who have met certain requirements and applied for a certificate of eligibility.

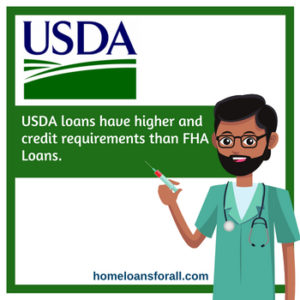

USDA home loans for nurses in MI

USDA nurse home loans in Michigan, which you may also see listed as Rural Development Loans, are loans that are paid out directly by the US Department of Agriculture to encourage prospective home buyers to move into more rural areas of the country.

This includes about 97 percent of the land in Michigan, including some areas you may not expect to qualify!

USDA loans have higher credit and income requirements than VA or FHA loans, but these requirements are still lower than those of most conventional mortgages.

Furthermore, these loans have longer lease periods, no interest rates, and (as you’ve no doubt guessed by their inclusion in this section) low to no down payments in most cases, making them a lot more affordable overall if you can get them.

The Detroit Neighborhood Initiative

If you live in the city of Detroit and are looking for home loan help, the Detroit Neighborhood Initiative is a home loan program that will provide you with a low interest fixed rate mortgage with no down payment on a new, existing, single-to-four family home, or condo within the city limits.

DNI loans have no minimum credit score and don’t even consider credit as a factor during the loan application process, making this one of the very best home loans for nurses with bad credit in Michigan.

Other home loans for nurses in Michigan

The most common option for nurse home loans in Michigan is what’s known as a “conventional home loan” or conventional mortgage. These loans usually come with high credit and income requirements and a 20 percent down payment, pricing them well out of what many Michigan nurses can afford.

If you’re looking for something more affordable, here’s some of the best government-sponsored mortgage programs available for nurses in the state of Michigan.

FHA home loans for Michigan nurses

FHA loans are similar to VA loans because both are insured by a government organization – in this case, the Federal Housing Administration. And because of that insurance, FHA loans have some of the most expanded eligibility requirements in the state of Michigan.

If you have a credit score of just 580 or higher, you will only have to make a 3.5 percent down payment on an FHA loan.

If your credit is lower than 580, your application may still get accepted if you can provide alternative forms of credit or if you are willing to pay a higher down payment of up to 10 percent.

Compared to the 20 percent down payment and 660-700 minimum credit scores required by moth conventional loans, FHA mortgages offer a great deal for Michigan nurses to take advantage of.

MI Home Loan

The Michigan State Housing Development Authority offers a home loan directly to citizens of the state that’s known as the “MI Home Loan.”

This is a 30-year mortgage with a fixed interest rate and a minimum credit requirement of 640. The biggest benefit of these loans is that the MSHDA will pay up to $7,500 of the down payment and closing costs for you.

The MSHDA also has a slight variation on this nurse home loans in Michigan called the MI Home Loan Flex.

The advantage of the Flex loan is that it’s offered anywhere in the state and to any home buyer who meets the credit and income requirements. The disadvantage is a minimum credit score of 660 instead of 640.

Conclusion – Nurse Home Loans Michigan

We hope that this article has helped you better understand how to find nurse home loans in Michigan.

With the help of the programs above you should be able to find a great loan option that works for you no matter what your budget or financial requirements look like. We know that sometimes finding a home can be frustrating, but get out there and start applying today!

by Mike Plambeck

Looking for Illinois home loans for single mothers can sometimes feel frustrating. Heck, looking for home loans in any situation can be frustrating.

You have to find the perfect house, shop around to find a lender who’ll give you good terms, and navigate the complicated paperwork. Then you have to cough up a huge down payment and find a way to afford the regular monthly payments.

When you’re also trying to raise a family on your own, all that can be overwhelming. That’s why we at Home Loans For All want to do everything we can to help.

Get Help Pre Qualifying for an Illinois Home Loan For Single Mothers – Click Here!

In this article, we’ll cover some of the best Illinois home loans for single mothers. We’ll explain why the conventional mortgage program might not be for you and then help explain the programs that are offered by the government at the state and federal levels.

Finally, we’ll cover some additional Illinois home buyer assistance for single moms that may help you get accepted or help you make payments on your mortgage.

Best Illinois home loans for single mothers

The basic Illinois home loan option is what’s known as a conventional home loan or conventional mortgage. Conventional home loans are expensive and inaccessible to many single mothers and home buyers with a less than upper-middle-class income.

The terms of most conventional home loans include:

- An initial down payment of 20 percent of the home’s total value

- A debt-to-income ratio of 40 percent or less

- A minimum credit score of 660 (some cases may even require a minimum credit score of 700!)

- Variable interest rates

- Payment of Private Mortgage Insurance every month for the first fifth of the payment period

The real killer here is the down payment. Even if you’re in a comfortable enough economic position to meet the credit and income requirements, and even if you’re confident about your ability to make monthly payments on a mortgage, being asked to pay thousands of dollars all at once is simply beyond the abilities of many home buyers.

Fortunately, there are MUCH better options for Illinois home loans for single mothers.

Welcome Home Illinois Loan Program

The “Welcome Home Illinois” home loan program is a 30-year fixed-rate mortgage with an interest rate that is guaranteed to be lower than the interest rate of a conventional home loan.

The income and credit requirements of the loan vary from lender to lender, and they’re certainly not as lenient as the loans we’ll talk about in the next two sections. However, they come with one major benefit: up to 7500 dollars worth of down payment assistance.

As long as you pay $1000 of the purchase price, you shouldn’t have to pay anything else up front. That makes this the perfect loan for anyone who knows they can handle the monthly payments but is concerned about paying thousands of dollars all at once.

Learn more about this helpful home loan for Illinois single moms here!

Illinois FHA loans for single mothers

FHA loans have long been one of the most popular programs amongst Illinois single mothers, and it’s not hard to see why. With low eligibility requirements, availability anywhere in the state, and fixed low interest rates, these loans are accessible and affordable.

If you have a credit score of 580 or higher, your down payment on an FHA loan will only be 3.5 percent of the total value of the home, which is much cheaper than the down payment on a conventional mortgage.

However, many lenders will accept credit as low as 500 for these types of loans, so long as you can also provide alternative forms of credit (like proof that you pay your utility bills regularly) or are willing to pay a slightly higher down payment.

The average terms of an FHA home loan for single mothers include:

- An initial down payment of 3.5 to 10 percent of the home’s total value, depending on your credit.

- A debt-to-income ratio of 50 percent or less

- A minimum credit score of 580 (500 in some cases)

- Fixed, low interest rates

- Payment of Private Mortgage Insurance every month for the entirety of the payment period.

Illinois VA loans for single mothers

VA loans are similar to FHA loans in that both are insured by a branch of a federal government, and that both have more lenient credit and income requirements as a result of that insurance.

For FHA loans, the organization involved is the Federal Housing Administration. For VA loans, it’s the Department of Veterans’ Affairs.

As you may have guessed, this means that these loans are only available to Illinois single mothers who are also former members of the armed forces. The lack of general availability is a disappointment, but the incredible terms of these loans more than make up for it.

In other words: if you can apply for a VA loan, you absolutely should!

The average terms of a VA home loan for Illinois single mothers include:

- NO initial down payment in most cases

- A debt-to-income ratio of 50 percent or less

- A minimum credit score of 500

- Fixed, low interest rates

- NO Private Mortgage Insurance payments

Illinois USDA loans for single mothers

USDA loans, also known as Rural Development loans, are designed to encourage prospective home buyers to move into rural areas of the state. For obvious reasons, those looking for a home in or around the city of Chicago need not even consider applying.

But for the rest of us, USDA loans are among the cheapest around even if they have stricter eligibility requirements than FHA or VA loans.

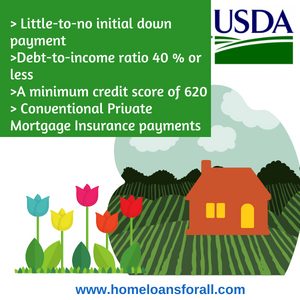

The average terms on USDA Illinois home loans for single mothers include:

- Little-to-no initial down payment

- A debt-to-income ratio of 40 percent or less

- A minimum credit score of 620

- Fixed, low interest rates

- Conventional Private Mortgage Insurance payments

Illinois home buyer assistance for single moms

Even if you’ve received one of the Illinois home loans for single mothers mentioned above, you may still require further assistance with making the payments or affording the home. Here’s some assistance offered by the government and by lenders that can help you afford home loans for single mothers in Illinois.

Firstly, once you’re paying off the home you can save money by taking advantage of the state’s homestead tax exemption. This allows you to withhold a certain amount of money from your property taxes while you’re living in a property that you are also paying off. In Illinois, this tax credit can save you up to $7000 in Cook County and up to $6,000 in all other counties.

Down payment assistance can also help you save money if you’ve been approved for a loan. The state of Illinois only offers down payment assistance in connection with certain mortgage programs (see our section on Welcome Home Illinois above for more info), but individual cities will often have down payment assistance programs in place.

Chicago’s Home Buyer Assistance Program for example, will offer low income home buyers (including single mothers) five percent of the value of the home in funds that can be used to pay off the down payment and/or the closing costs on a mortgage.

Take a look in your own area and see what programs are available!

Assistance for single moms with bad credit

Credit is the first thing a lender looks at when they decide to approve or reject your mortgage application. So when you have bad credit, it can be very difficult to find Illinois home loans for single mothers.

One thing you can do to find a home loan with bad credit is to seek out a co-signer. A co-signer is a relative or close friend who agrees to tie their credit to your property, allowing you to apply for the mortgage as though you had better credit than you actually do.

This makes it easier to get Illinois home loans for single moms and will also give you better terms on the loan once you’ve been accepted. However, the co-signer absorbs a lot of risk and may be asked to help make a mortgage payment if you miss a month.

If you can’t find a co-signer and absolutely cannot afford a home loan, you might want to try a rent-to-own contract instead. This lets you apply for a rental contract in the short-term (with the lower credit requirements and cheaper payments that implies) for a property that you can later buy outright.

Finally, you can always try to repair your credit. Conventional wisdom will tell you that you can only do this with the help of an agency, but that is simply not true. There is nothing that a credit repair agency can do for you that you cannot do for yourself by paying your bills, reducing your debts, and applying for secured credit cards.

You can learn more about how single mothers in Illinois can repair their credit by reading this article.

Conclusion

Illinois home loans for single mothers aren’t too hard to find when you know where to look. Even if a conventional mortgage is beyond your reach, you might be able to find a lender offering FHA, VA, or USDA loans who’s more willing to work with your financial needs.

Single mothers deserve our respect, our admiration – and perhaps most importantly, they deserve to live safely and securely in a permanent home of their own.

by Mike Plambeck

Many states have special programs in place to help paramedics, police officers, EMTs, firefighters, and/or certified first responders find homes. Sadly, Georgia is not one of them. We understand that without this kind of help it can be difficult to find a mortgage – it takes a lot of time, which most first responders may not have, and a lot of money – ditto.

However, there are still great first responder home loans in Georgia if you know where to look.

Get Help Pre Qualifying for a First Responder Home Loan In Georgia – Click Here!

In this article, we’ll cover some of the federal and state level home loan programs that can help Georgia first responders find a home in a good area at an affordable price. We’ll also cover what to do if you have bad credit or low income.

At Home Loans For All, we firmly believe that everyone deserves to live in a safe and permanent home and shouldn’t have to settle for an apartment or duplex, no matter what their financial situation may look like.

Let’s dive in and start looking at some great Georgia first responder home loans!

Best First Responder Home Loans in Georgia

The basic home loan program offered in Georgia, as you may be already aware, is what’s called a conventional mortgage.

Conventional mortgages aren’t bad, per se, but they’re definitely targeted towards the upper-middle-class. Some Georgia first responders may be able to afford these loans, but many will not.

The basic terms of a conventional mortgage are a minimum credit score of 660 to 700, a debt-to-income ratio of 40 percent or less, upper-middle income, non-fixed interest rates, the regular payment of Private Mortgage Insurance (PMI), and an upfront down payment of 20 percent of the home’s total value.

Even if you meet the credit and income requirements, that down payment is a real problem for many home buyers. Just because you can afford to make a few hundred dollars towards a weekly payment doesn’t mean that you can afford to pay thousands of dollars all at once, right?

Here are three other first responder home loans in Georgia that you may find more accessible.

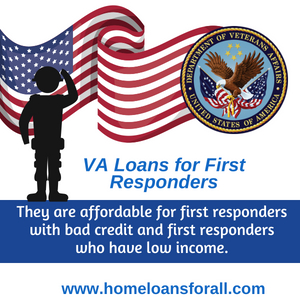

VA loans for GA first responders

VA home loans are insured by the Department of Veterans’ Affairs. As you can probably guess, this means that they are only available to former members of the armed services who have received a VA Certificate of Eligibility.

However, since many Georgia first responders are ex-military, many of our readers may be able to take advantage of this extremely beneficial mortgage program.

Because these loans are partially backed by the federal government, private lenders see them as having much less risk than a conventional mortgage.

This means that they are willing to take on “riskier” prospects and may even give Georgia first responder home loans to applicants who would normally be rejected outright.

Also, by not requiring a down payment (in most cases) or PMI (in all cases), these loans will save any loan buyer lucky enough to secure them thousands of dollars on the mortgage.

The average terms of a VA home loan include no down payment, no private mortgage insurance, no minimum credit requirement (though lenders will often set their minimum credit requirements of 500-580), no minimum income provided you have a debt-to-income ratio of 50 percent or less, and fixed low-interest rates.

FHA loans for GA first responders

FHA loans are becoming one of the most popular programs in Georgia, and when you look at the benefits of these mortgages, it’s not hard to see why.

With low credit requirements and the fact that they’re offered anywhere in the state, they’re much more accessible than either the conventional mortgage or VA mortgage programs.

Plus, while the individual monthly payments are sometimes slightly higher than they would be for a conventional loan (due to the PMI requirements), the initial cost of the down payment is much lower, and usually, you save money on an FHA loan over time.

The average terms of an FHA first responder home loans in Georgia include a down payment of 3.5 to 10 percent (depending on credit), a minimum credit requirement of only 500, no minimum income provided you have a debt-to-income ratio of 50 percent or less, Private Mortgage Insurance payments for the duration of the loan, and fixed low-interest rates. Learn more here.

USDA loans for GA first responders

USDA Rural Development first responder home loans in Georgia are designed to encourage people to move into rural areas of the country. Approximately 97 percent of land in the state is eligible for this kind of mortgage, so consider applying even if you think you live in a suburb of a big city!

USDA loans aren’t quite as accessible as FHA loans, but they can save you money in the long run. The average terms of a USDA loan in Georgia include low to no down payment, a minimum credit score of 600, less than 115 percent of the median income for the area, and conventional Private Mortgage Insurance payments. USDA loans usually also have some of the lowest interest rates around.

Georgia mortgages for first responders with bad credit

Your credit score is seen as the ultimate measure of your financial responsibility. If you have bad credit, it suggests to mortgage brokers in Georgia that you might not pay back the money they lend you and makes it much more difficult to secure a good home loan.

Of course, we know that sometimes bad credit happens to good people. So besides taking advantage of FHA and VA home loans, here are some other options to pursue in you’re looking for first responder home loans in Georgia and you have bad credit.

Getting accepted

The easiest way to get a home loan when you have bad credit is to seek the help of a co-signer. Finding a cosigner is an option that’s especially popular with first time home buyers, graduates, and newlyweds – people who want to own a house but who may not have had time to build a good credit score.

A cosigner’s credit score will boost your own, allowing you to apply as though you have better credit than you actually do. This will lead to better terms, lower down payments, and a better chance of getting accepted. You can even find a cosigner for an FHA or VA loan to save even more money!

However, the cosigner will be absorbing a lot of the risk by tying their credit directly to your property. In some cases, they may be approached to make payments if you miss a month.

So make sure that your cosigner is someone you can trust and that they trust you in return before entering into this kind of agreement!

Another thing to remember is that mortgage brokers can manually underwrite any of the requirements on a home loan. So they can lower the credit requirements or get rid of the down payment entirely.

They usually only do this in special cases, and often require proof that your current financial situation is not your fault, but they may be willing to give special consideration to Georgia first responders. Speak with your lender today and see what they can do for you!

Dealing With The Down Payment

Many buyers find that the hardest part of buying a house is affording the steep down payment. This is especially true when you’re trying to find first responder home loans in Georgia with bad credit.

A bad credit home buyer is seen as a higher risk, so even if it’s an FHA loan, lenders will usually expect you to make a higher down payment so that they know that they will make at least some of their money back up front.

This is when you might start needing to look at the down payment assistance programs offered by the state. If you apply for a Georgia Dream Home Loan through the Georgia Department of Community Affairs (GADCA), the state will pay up to $7,500 of the down payment for you as long as you still pay at least $1,000 yourself.

Conclusion

We hope that this article has helped you better understand how and where to find first responder home loans in Georgia. At Home Loans For All, we believe that everyone deserves to live in a safe, comfortable, and permanent place of their own no matter what their finances look like.

And until the state of Georgia gives first responders the respect and assistance they deserve, we’ll do everything we can to help you find Georgia mortgages for first responders!