How much can veterans expect to pay for the VA appraisal fees? This inspection is a necessary part of the home buying process for individuals who want to take advantage of the features found in a VA mortgage. Ideally, this ensures that the property meets the minimum standards of safety and sanitation. You should know what this process is going to cost you, especially because it isn’t something you can get out of paying.

Indeed, the VA appraisal fee schedule isn’t usually set in stone. The fees can vary based on where your home is located and the type of home you’re attempting to purchase. However, most veterans will pay between $300 and $500 for their VA appraisal fees.

The good news is that you might be able to ask the seller to repay these costs as a part of your negotiations.

Get Help Pre Qualifying for a VA Home Loan – Click Here!

This upfront fee applies to your initial appraisal and home inspection. If something is identified as needing repair, the appraiser may make a note of it and schedule another inspection at a later date once the issue has been resolved. You might find that the VA appraisal fee schedule adds up quite quickly when you have significant repairs that need taken care of.

What are Non-Allowable VA Appraisal Fees?

Veterans only should pay for certain items when they purchase a new home, including:

Discount points to lower their interest rate

Reasonable fees for itemized items and charges allowed by the VA

Lender’s one percent fee

Under this loan program, there are some costs that a veteran should not have to cover during the purchase of their new home. These are commonly referred to as “non-allowable fees”. Some of the most important items to note on this list include:

Processing fees

Document preparation fees

Interest rate lock-ins

Lender appraisals

Postage

Notary fees

Tax services

All of these items must be covered under the lender’s one percent fee or the veteran is not responsible for them. This prevents the buyer from paying for excessive charges that truly have no benefit to their process. Lenders must keep an important check on how much they charge; it is going to come in under that one percent mark.

Who Pays the VA Appraisal Fees?

In terms of the VA appraisals, some of these non-allowable fees relate to who orders a particular appraisal and the reason for the order. Only the borrower or the lender can request the initial appraisal unless someone else is going to cover the cost. Under normal circumstances, the buyer pays for the appraisal fees.

Show them this website, so they know who they are working with. We will not allow them to trick you!

The seller and lender may sometimes argue that an additional appraisal is necessary for the sale of the home. They are well within their rights to request an appraisal. BUT they cannot demand that the veteran foot the bill for that additional expense.

The same principle applies to a reconsideration of value. If the buyer agrees to order and pay for a new appraisal to see if the house will appraise at a higher rate, it is acceptable to order an additional VA appraisal. However, the lender and the seller cannot demand that the veteran pays for an entirely new appraisal.

The intent behind this policy is to prevent veterans from paying for unnecessary services that only benefit the lender or the seller. Their end goal is to sell the home or to make money from your financing. So, they have something to gain from the home receiving a higher appraisal. Any disagreement they have with the actual appraised value might not be entirely honest. This prevents the veteran from having to pay for their attempts to sell the home at a higher rate.

This last non-allowable fee should go without saying, but borrowers shouldn’t pay for services they didn’t get. Sometimes, you may have an appraiser or an inspector attempt to add fees to the sale of the home (Horrible!). Veterans must be charged fairly for the work that is done on the property. So, you should actually receive something in exchange for your money.

What is the VA Appraisal Fee Schedule?

The VA appraisal fee schedule varies based on your location. It might even vary based on the type of property you are attempting to purchase. For the specific details regarding what the VA appraisal fees in your state are, you can view this map from the Department of Veterans Affairs. By clicking on your state, you can see the fee schedule for your area and your property type.

In short, this fee schedule is the timeline you can expect from your VA appraiser. Most areas estimate that the timeline is approximately ten days or less. The exception to this is in more remote areas such as Alaska. There might be more travel time involved or fewer inspectors available to survey the property.

VA Appraisal Fees

The VA appraisal fees are a necessity when purchasing a home using this advantageous program. You should know what to expect from the VA appraisal fee schedule. There are things they should not charge you for. Educating yourself on the process right now is the best way to ensure that you only pay the recommended amount when the time comes.

Frequently Asked Questions

Who pays VA appraisal fees?

The buyer pays the VA appraisal fees but the seller may be able to repay these fees during negotiations. Learn more about VA buyer and seller requirements by clicking here.

How can I get a VA appraisal fee waiver?

All properties will need a VA appraisal, and there are no VA appraisal fee waivers.

Can I get a VA appraisal fee refund?

No, you cannot get a refund once the appraisal is officially completed. However, you may ask the seller to repay the costs at closing depending on your negotiations.

Are there any VA appraisal fee limits?

Yes, there are limits to the VA appraisal fees. Be sure to check what the limits are in your local area with the VA website here.

When you purchase a home using a VA mortgage, every eligible property has to pass the VA appraisal and inspection process. The Department of Veterans Affairs has a list of minimum property requirements in place to help protect veterans from purchasing a financially draining new home. All of the standards relate directly to the safety and sanitation of the property rather than to cosmetic standards. The VA roof requirements are a subsection of this appraisal, allowing you to take a closer look at what happens to be on top of your new home.

There are some unique roof requirements that apply to VA loans, even though this may not always be the case with conventional mortgages. The VA roof requirements are much more stringent in order to protect the veterans who are considering purchasing these properties. A private lender with a conventional mortgage might be able to overlook some of the more minor issues that would derail a VA loan.

Get Help Pre Qualifying for a VA Low Credit Home Loan – Click Here!

To prevent a potential holdup with your financing, it might be necessary to take a closer look at whether your property will meet the VA roof requirements or not.

What is on the VA Loan Roof Inspection Checklist?

Your appraiser has a long list of items they are required to look for during the walkthrough of your property. The roof is simply another item on their list. What exactly is included in their VA loan roof inspection?

The exact specifications for the roof are found in the VA Pamphlet 26-7, specifically in the Lender’s Handbook in Chapter 12 under the Minimum Property Requirements. Appraisers are really evaluating the roof for two very specific criteria. Does it prevent the entrance of moisture? Does it provide reasonable future utility, durability, and economy of maintenance?

There are no other specific criteria that show specifically which roofs will pass a VA home inspection. Some of this the appraiser will have to consider to determine what constitutes an issue with your unique property.

Prevent Entrance of Moisture

All homeowners would agree that the roof’s primary function is to keep the elements at bay. You wouldn’t want to purchase a home that already has extensive water stains on the ceiling from an active leak. The ceiling might be bowed from the weight of all the water or it could just be small brown patches that indicate some moisture was recently there. Either way, the appraiser takes this entrance of moisture very seriously.

The roof on a particular home should be able to prevent moisture from entering your living spaces without much effort. If the room is already demonstrating that it can’t handle a rainstorm, the problem will worsen over the coming months or years. This can devolve into an expensive issue not too far down the road. This brings us to our very next point.

Provide Reasonable Future Utility, Durability, and Economy of Maintenance

An appraiser wants to see that the roof on your new prospective property is likely to withstand at least two years’ worth of daily wear and tear. That means that most of the shingles should be in place with no leaks on the inside. Any other signs that the roof could be in disrepair are also red flags to an appraiser, including sagging.

This standard is to protect you as the home buyer from purchasing a home that already needs an expensive repair upfront. This can help to protect your financial interests long-term. So, you can avoid shelling out for a roof that costs thousands of dollars immediately.

You may be able to have the roof replaced and still move forward with the financing for this property. Keep in mind that if the property has more than three layers of shingles, they must all be removed and replaced before the replacement.

These are the standards for the VA loan roof inspection. However, remember that the home needs to comply with local building standards first and foremost. Any extra standards imposed by the VA should be secondary to these codes.

How Can I Get the VA Roof Certification?

If the appraiser notes anything odd about your roof, you may be asked to get an additional VA roof certification. These are not always necessary. BUT you might want to consider getting one if you believe that your financing might otherwise be derailed by the roof. They can recommend more detailed repairs and a future course of action for the property.

A roof certification is a detailed inspection of the current state of the roof by a licensed specialist. This is different than your home inspector and appraiser. They do not typically have the experience and know-how to issue a thorough VA roof inspection. These experts look at the condition of the roof, including any movement, the soundness of the flashing, and even the gutters and downspouts.

When there are no repairs needed, they are generally asked to estimate the remaining lifespan of the roof. For a VA loan, the lender wants to see that it should last a minimum of two years.

Who Issues the Roof Certification?

A professional roofer will issue your roof certification. They might be able to issue this guarantee immediately, as long as there were no repairs necessary to the property. On the other hand, the company should be able to issue a roofing certification after they perform any of the repairs.

This certification should be good for two to five years, depending on your area and the lifespan of the roof.

VA Roof Requirements

Passing a VA loan roof inspection doesn’t have to be difficult or worrisome. Those VA roof requirements are to make sure that you purchase a home that is safe for the years ahead. Consider the inspection and the guidelines set out in the VA pamphlet 26-7 as an excellent lens through which to view potential properties. After all, would you really want to purchase a home that didn’t meet the VA roof requirements?

Take a look at some other Common VA Appraisal Problems by reading our article here.

Applying for the beneficial VA home loan program comes with its own set of specific VA loan requirements and criteria for both the buyer and the seller.

Both parties should be well informed about what to expect throughout the process to equip you to make better decisions. The entire process can move smoother if you anticipate what the lenders will require of you in advance.

VA Loan Requirements: What Buyers Should KNow

For buyers, the requirements are relatively simple. You must obtain your Certificate of Eligibility that proves you met the service requirements necessary for the Department of Veterans Affairs entitlement.

There are multiple ways to go about obtaining your COE, including allowing your lender to do the work for you, mailing away for it, or completing it through the eBenefits portal.

You can find more information on how to receive your Certificate of Eligibility here.

Beyond the specific criteria for a VA home loan, you will also need to meet the financing requirements set out by your lender.

The financing is partly guaranteed and backed by the Department of Veterans Affairs, but they are not responsible for issuing the loans.

You will need to find a private lender at a local bank or mortgage broker for financing. Click here to pre-qualify today!

As a result, the financing requirements can vary based on the lender you select. These requirements could include a minimum credit score, certain income requirements, and a reasonable debt-to-income ratio.

You must also select a property that is eligible for the loan and can pass the appraisal process.

VA Loan Requirements: Important Seller Information

Sellers will encounter far fewer requirements with the VA loan program. In fact, they face almost none of the paperwork or red tape that buyers will occasionally encounter. They may face higher costs when it comes to selling the home to a VA buyer though.

For example, the VA has certain non-allowable fees which limit which services and costs can be passed onto the buyer. This is designed to help lower the overall cost of homeownership for veterans.

The processing or underwriting fee may be waived on a VA home loan or the seller will foot the bill for it. In addition, you may be responsible for paying the settlement or closing fee.

Combined, these costs could add up to almost $3,000.

The home must also meet certain criteria that fall under the minimum property requirements set out by the program. This will be determined through an appraisal by a third-party VA loan appraiser.

As a seller, you do maintain the right to refuse an offer on your home based on their approved financing through the VA loan program.

Discrimination against VA loans is illegal!

You cannot simply disregard an offer simply because the buyer is a veteran, however you can negotiate a deal that is much more favorable based on the estimated costs you will face as the seller.

How Do VA Loans Work

Receiving a VA home loan means that you may be able to save thousands of dollars on your mortgage compared to traditional financing options. You may find that the process works a little differently than you would expect.

The Department of Veterans Affairs backs each loan in part with a maximum eligibility of $36,000.

This hefty sum often replaces the need for the traditional down payment that once provided peace of mind to the lender. Instead, the VA is offering up their own funds as security on the loan. Lenders are able to offer more favorable terms due to the security this government backing affords to them.

Buyers can greatly benefit from the lender’s security in the loan. This means that lenders may be willing to take a greater risk on individuals and families who don’t meet their standard profile for conventional financing.

The lender may be more apt to approve clients with a slightly lower credit score or a higher debt-to-income ratio.

VA Loan Benefits for Buyers

You will also receive a couple of major perks to financing a new home through the VA loan program.

In most circumstances, buyers are not required to place a down payment on the home. This automatically becomes the source of the most significant savings for prospective home buyers.

They may have previously spent years scraping together a savings account large enough to accommodate a twenty percent down payment.

By waiving this massive sum, homeownership can become a reality on a much shorter timeline.

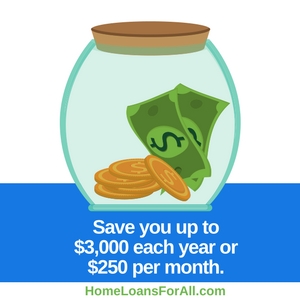

Conventional financing also requires borrowers to pay private mortgage insurance (PMI) on any loan that has a down payment of less than twenty percent.

This fee is waived on a VA home loan as a result of the guarantee issued by the federal government.

Not paying PMI can mean a significant source of savings for you on a monthly basis.

Consider that the average home in the United States costs roughly $200,000. Private mortgage insurance runs between 0.3 percent to 1.5 percent of the home’s value on an annual basis.

This could save you up to $3,000 each year or $250 per month.

Buyer Requirements

Before you start entering into the process of purchasing a home with a VA loan, you should be aware of all the buyer requirements.

This is an incredibly beneficial program, but it does have certain standards that must be upheld if you would like to receive financing.

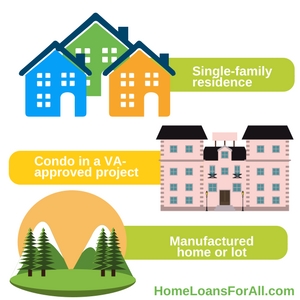

The biggest requirement is that you must find a property that meets the minimum property standards.

The loan itself is relatively flexible on the type of home that you can purchase with this financing. For example, you can purchase any of the following property types:

Single-family residence

Condo in a VA-approved project

Manufactured home or lot

No matter which type of property you plan to purchase, they must all meet the criteria set out by a VA appraiser.

These criteria are known as the minimum property standards, sometimes abbreviated as the MPS. The majority of the requirements are in place to ensure that veterans are purchasing homes that are safe and sanitary.

During the appraisal process, your independent appraiser will be looking for key issues with the property in areas including:

Clean running water

A working sewage system

Adequate heating

Issues with the electrical system or other mechanics

Roofing condition

Termite inspection

It should be noted that an appraisal differs from a thorough property inspection. While it may catch some major issues with the property’s safety into the foreseeable future, the appraisal is only a general glimpse at the living conditions.

An inspection is much more thorough with an eye for detail in many of these systems.

Credit Qualifications

One of the key questions regarding the buyer requirements is related to the credit score necessary for financing. The good news for many prospective applicants is that there are no minimum credit scores required to receive a VA home loan.

Instead, lenders are encouraged to take a look at your entire profile before making a decision on whether to issue you a loan.

The minimum credit score any particular lender will accept can vary widely. Some will have their own benchmark scores that they use for determining approvals.

However, if you can find a lender that is willing to work with your credit score, the VA will still back the loan. This presents the opportunity for prospective applicants to receive financing even if they have poor credit.

If you don’t qualify for one lender, don’t be afraid to apply for a VA loan at another lender. You may be surprised to receive a different answer.

Seller Requirements

Many sellers are hesitant to accept offers from buyers who plan to use the VA loan financing. There are a lot of misconceptions regarding how the process works for financing and what the seller VA loan requirements are.

Fortunately, there are very few requirements placed upon sellers who accept an offer through the VA loan program.

One of the largest myths regarding the buying process is the turnaround time. They believe that the turnaround time on loans will be much longer than that of conventional financing.

However, the new and more refined VA loan program is more streamlined than it was in the past. Many of the processes now are done through the online portals instead of through the much slower process of using the United States postal service.

Currently, the average turnaround time on a closing is just 43 days compared to the months that many sellers anticipate.

You will also want to use a great listing agent who is familiar with what the minimum property requirements will be. They should be able to advise you if the home will meet the standards that appraisers are searching for with the VA loan requirements. If your home is a massive fixer-upper, you may need to consider that the home is a better fit for the FHA 203k loan.

The other major component to accepting VA financing is that you may be responsible for some of the “non-allowable fees” on the loan. The amount of money and fees that you will be charged based on the loan will be dependent on the lender.

Some of the fees may be waived by the lender or passed onto you as the seller. These can include a processing or underwriting fee, as well as the escrow, settlement, or closing fee.

VA Loans Restrictions

While there are many advantages of the VA loans, there are some restrictions placed upon buyers for the type of properties and fees that are eligible.

Property Restrictions

The type of properties that qualify for a VA loan is rather extensive, ranging from single-family homes to manufactured homes to condominiums in a VA-approved project. You can even purchase modular homes or build your own home. The only major restrictions are vacant land and co-ops.

However, this doesn’t mean that every property that falls into one of these categories is going to qualify for a VA loan.

It must still meet all of the minimum property requirements during the appraisal process. They will be looking for homes that provide adequate living space in a safe and sanitary environment.

These can include standards such as issues with running water, electrical problems, roofing disrepair, and other key issues that could be integral to the health and safety of the property.

Keep in mind that you may discover issues with the home during an inspection that are not present during the appraisal.

These will not necessarily prevent you from purchasing the home, but they should be taken into consideration before you make a final decision.

Title Restrictions

You will have a difficult time meeting the VA loan requirements if there are going to be title restrictions on the new property. These restrictions can include anything that would make it difficult or impossible for the new homeowner to sell the property at will.

They should be able to sell the home on the real estate market whenever they desire, without the approval of a homeowner’s association or condo project approval.

If your new loan comes with a “right of first refusal” or other title restriction, your financing could be in jeopardy. These restrictions must be disclosed before closing and may be evaluated during the appraisal process.

Closing Cost Restrictions

When it comes to making your purchase official, there are lots of restrictions on what veterans can and cannot pay for.

These closing cost restrictions apply to the overall bills associated with attorney’s fees, underwriting, escrow fees, processing, documents, and tax services. Bills that fall into these categories are considered “non-allowable” and must be handled differently.

The most common method of paying these bills is to pass them onto the seller. You may include the necessity of covering these charges directly in the offer you make to the seller.

This allows the seller concessions (the money they contribute to the closing costs and purchase of the home) to be included in your contract.

It should be noted that a seller can only contribute up to four percent of the purchase price of the house.

The money can be used to cover the closing costs or the funding fee required for a VA home loan.

The real estate agent may also cover a portion of these costs in some states based on the percentage of commission they will make from the sale.

In other situations, the lender can waive or reduce the overall closing costs. They may also bundle some of them into an origination fee that can be paid by the borrower.

VA Loan Requirements FAQs

Is there a minimum credit score for a VA loan?

There is no minimum credit score for a VA loan. The minimum credit score for a VA home loan is set by the individual lenders who will issue the financing.

The financial backing of the government encourages lenders to take a look at the entire profile of a prospective applicant instead of basing decisions on credit scores alone. If you can find a lender who is willing to work with you, the VA will still guarantee the loan.

Do I qualify for a VA loan with a general discharge?

Yes, you can qualify for a VA loan with a general discharge. You can qualify with anything other than dishonorable discharge.

How many times can you use a VA loan?

You can use the VA loan multiple times as long as the entitlement is paid back.

Do You Have to Pay PMI on a VA Loan?

VA loans do not require private mortgage insurance or PMI. This can mean substantial savings compared to more conventional forms of financing.

How do I get a VA loan Certificate of Eligibility?

You can receive a VA loan Certificate of Eligibility by applying through your lender, through the eBenefits portal, or in the mail.

With online applications for the COE, you may receive a response in just seconds or minutes.

You must meet the service requirements that are set out by the Department of Veterans Affairs, including the length of service and other than dishonorable discharge. You can view the full list of requirements to receive a VA loan in our article here.

Conclusion

The benefits of obtaining a VA loan are far-reaching and have the potential to save you thousands of dollars over the course of your loan. Particularly for buyers, you can experience the advantages quickly and easily if you meet the VA loan requirements.

Sellers will have few responsibilities apart from ensuring the safety and sanitation of the property.

Knowing what to expect in advance can help you to make a wiser decision on the purchase of a home, as well as to anticipate the rest of the process.

You can start preparing for the purchase of a new home by looking over the VA loan requirements today.

Purchasing a new home with a VA loan requires your home to pass the appraisal process instead of falling victim to some of the common VA appraisal problems. Unfortunately, not every property will be able to adhere to the stringent guidelines set out by the program.

This can be easily avoided by selecting a safe property, but it also helps if potential homebuyers can anticipate some of these common VA appraisal problems during their shopping period.

You Might Already Be Pre-Qualified For A VA Loan In Your State – Click Here!

The Department of Veterans Affairs (VA) agrees to back a portion of every loan using federal funding. Their guarantee makes private lenders more likely to issue loans with more favorable terms and financially advantageous features to veterans and active duty service members.

Because the government is agreeing to back these mortgages, they also want to ensure that their own interests in the property are protected by the VA appraisal process.

In a VA appraisal, a third-party inspector is hired by the government to take a look at a prospective property for home buyers. This person is checking to ensure that the home meets the minimum property requirements that make it safe and sanitary for veterans to live in long-term.

A home that fails to meet the requirements according to the appraiser’s findings will no longer be eligible for the VA home loan until those issues are corrected.

What Are the Common VA Appraisal Problems?

Every property that is purchased using a VA home loan must meet certain minimum property requirements (MPRs). These items ultimately comprise the VA appraisal checklist.

These are qualities that prove that the home is safe and sanitary for a veteran to live in. While it may seem like a few of these characteristics are relatively arbitrary, homebuyers should actually be grateful they exist. This is the government’s way of helping to protect homeowners from purchasing a house that could potentially be a money pit or unfit for veterans to live in.

Some of the minimum property requirements are relatively easy to guess: the home must have no obvious safety issues, have adequate living space, must be zoned for residential use, and essential systems must be in great working order. For a more extensive list of the MPRs that an appraiser will be looking for, see the list below:

Adequate heating

No electrical or plumbing problems

Clean drinking water

No roof issues

No lead paints

No termite or pest infestations

No obvious issues with the infrastructure or defective construction

Property accessibility

Within each of these categories, there are a few common VA appraisal problems that homeowners face. For more information on what issues could jeopardize your funding, you can see the breakdown of some of these common issues below.

Common VA Appraisal Problems

Mold and Mildew: Mold can be particularly hazardous to your health, even with just short-term exposure. The VA appraiser is going to be keeping an eye out for any mold spores or mildew growth that could the sign of a much larger moisture issue.

Exposed Wires: Have you ever looked at a home that had bare wires and felt good about the state of its electrical system? Most appraisers and inspectors will immediately flag a home that shows signs of electrical disarray. These issues can be extremely expensive to repair and could lead to major issues like fires.

Check around, particularly near the breaker box, to make sure nothing stands out to you or you could be facing one of these common VA appraisal problems.

Windows: Windows are an important part of a home because they allow ventilation and serve as a secondary means of escape during emergencies. Perhaps this is why appraisers will be checking to ensure that they are all in fully operable condition.

They should be able to open and the panes should be free of major cracks or chips. A missing pane will definitely raise some red flags for an appraiser. This is an item you can investigate before you ever even complete a walkthrough of the home to help you avoid this common issue.

Insufficient HVAC: Not all areas are required to maintain both heating and air conditioning. However, heating is a priority and a must-have feature in every home. Even if you don’t feel like the heat is completely necessary, a non-functioning furnace will derail a VA appraisal.

This prevents you from being able to maintain a comfortable living condition in the event of a winter disaster.

Roofing Problems: Did you notice that steady drip that comes straight from the ceiling? Whether you can tell there are shingles loose or you can see the beginning of a major roof leak, a VA appraiser is going to take a relatively thorough look at the roof.

After all, this is what protects the entire home from the elements and windy weather. If you see a roof problem, it is most likely going to need to be corrected before you can close on the home.

What Should I Do if the Home Fails the VA Appraisal?

If the home fails the VA appraisal, that doesn’t necessarily mean that all hope is lost. You have a few alternative options to secure the funding you need to make the home your own.

However, you will have to ensure that any issues raised by the appraiser are corrected before the lender is going to issue the financing you need to purchase the property.

You can definitely request that the seller make the necessary repairs before you’re willing to close on the property. Some sellers are more than willing to make the much-needed repairs in order to secure a buyer for their home. However, others may still hold out hope that they can sell the home without sinking another penny into its cost and maintenance.

If this describes your seller, you might choose to pay for the cost of the repairs yourself. This is a risky endeavor because you will be putting money into a home that you do not yet own.

Using this method, you can ensure that the home receives the repairs it needs from a contractor of your own choosing while still securing your financing. Unfortunately, these funds must be paid for upfront without the ability to bundle them into your principal loan balance. This isn’t a financial possibility for many prospective home buyers.

If the property simply doesn’t appraise for the value of the sale price, you can ask for a Reconsideration of Value and challenge the VA appraisal. It is possible that the appraiser either made a mistake on the square footage of the home or didn’t account for any recent upgrades to the property.

In other situations, they may not have used truly comparable real estate listings to make their comparison for value. For more information on how to challenge a VA appraisal, you can see our article on it here.

Last but not least, you can choose to walk away from the property altogether. If your appraiser identified a lot of major issues that will come with a significant repair bill, you might want to consider whether you can afford to repair and maintain this property long-term.

More repairs might be coming after you finish covering the cost of these, and that is just to meet the minimum property requirements. Walking away could save you more in the long run.

Conclusion

The VA appraisal process exists to help protect veterans from purchasing homes that will cost them a small fortune in repairs. While there are quite a few standards set in order for a home to meet the minimum property requirements on the VA appraisal checklist, they are all ultimately in the best interest of the veteran purchasing the home.

If you encounter any of these common VA appraisal problems, your financing is likely to be derailed until you can have them remedied.

The solution to your common VA appraisal problems may not always be entirely clear. You will have to weigh all of the options based on the issues at hand before you make a decision. Be sure to talk with your lender about any of these issues that might show up on your upcoming appraisal.

Frequently Asked Questions

How long does it take for my VA appraisal to come back?

It should take approximately ten business days or less to put together the full report from your VA appraisal. It may take longer in areas that have fewer independent inspectors to complete the task.

How much does a VA appraisal cost?

A VA appraisal is the responsibility of the buyer and it usually costs between $300 and $500.

How much does it cost to challenge a VA appraisal?

There is no cost to challenge a VA appraisal. This is simply a review of the previous appraisal alongside any new or differing data from the first visit. Unless there is a request for an increase of 10 percent value or more, there is no need for an additional walkthrough.

Many prospective home buyers are more interested in purchasing a condo with their VA loan than a detached home, but they aren’t sure if it’s possible.

The good news is that you can purchase a VA approved condo with a VA mortgage, but you will face additional challenges. As long as you are prepared in advance for the challenges you could potentially encounter, purchasing a condo with your VA loan could be a smart move financially.

VA loans are one of the best programs available because they feature no down payment, no private mortgage insurance, and low interest rates.

We Can Help You Qualify For VA Approved Condo Loan

Fill Out The Form Below To Get Help Today!

It’s rare to find this combination of terms in other loan programs, so eligible service members and veterans should highly consider taking advantage of it.

Over the course of your loan, this type of mortgage could save you thousands of dollars.

What are VA Approved Condos?

One of the biggest questions facing potential buyers is what VA approved condos actually are. While there are all types of properties that are VA approved, the Department of Veterans Affairs doesn’t actually approve each individual condo unit, but they do take an overarching look at the complex where the unit is located. Their goal is to help veterans and service members to purchase a home that will meet all of their needs long-term, including when you may need to resell it in the future.

As a result, they are interested in seeing how the complex actually functions. They want to make sure that there are no restrictions on the resale of the property, the details of the HOA, and even how the budget is spent on their community. VA approved condos are located within a complex that should be beneficial to veterans in the long run.

The individual unit will still need the appraisal to receive final financing through this program.

Benefits of Purchasing a Condo

Some homebuyers aren’t really sure what they can gain from purchasing a VA approved condo instead of a traditional single-family home. Going through the approval process for a condo or a townhouse can be extremely difficult and time-consuming. Do the benefits of purchasing this type of property outweigh the disadvantages and frustration of getting the property approved?

Condominiums and townhouses can be a great way to receive additional perks to your living situation at no additional cost. Many of these communities provide the same benefits as an apartment complex, including pools or gyms.

High-end neighborhoods and complexes might even have a clubhouse where they host exclusive events on a regular basis. Some residents prefer the fact that the community takes care of their yard work and maintenance for them as well.

Instead of renting an apartment, you could be putting your monthly housing expenses into a wiser investment. The money you spend can build equity in your home that could pay off in the future.

Be sure to consider whether you can afford to maintain one of these condominiums before you purchase it, but it could be a financially savvy move for you.

The best way to take advantage of all these perks is to find a unit within a pre-approved VA project. This reduces the headache of securing all of the documentation necessary for the VA to review and issue a final approval on a condo.

If you aren’t in a hurry to move into your new home, you might even find that it’s worth it to move through the VA approval process.

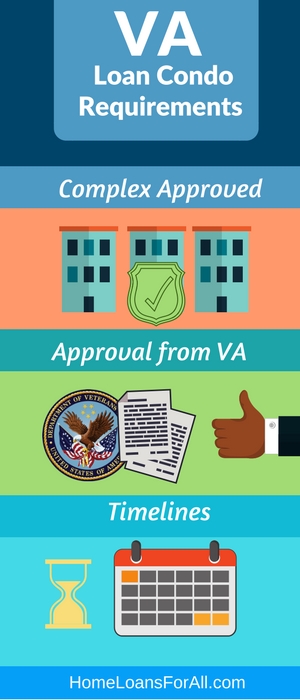

What are the VA Loan Condo Requirements?

Finding a condo that meets all of the VA requirements is the first hurdle you will encounter with your purchase. You should know upfront exactly what the VA requires from a condo and the neighborhood where it is located before you become too attached to a specific unit. Take a look at these guidelines to help you meet all of the requirements.

Complex must be approved.

The VA does not allow veterans to purchase condos that aren’t on their list of approved complexes. Their approval means that they have already reviewed the covenants, bylaws, and other factors that could potentially limit your home’s resale value in the future. Their restrictions on complex approval are ultimately designed to benefit homeowners in the long run, even if they seem inconvenient right now.

Check the VA approved condo database to determine if the complex you are interested in is already accepted. If you don’t see it in this database, you should check to see if it is approved by HUD or the USDA. It’s possible that the VA will accept a complex that already has the approval of these two agencies as long as it was granted before December of 2009.

Ask the lender to seek approval from the VA

Sometimes, you might find that you fall in love with a condo that isn’t on the list of approved properties. You can always ask the lender to seek approval from the VA, but it could be a time-consuming process. The lender will need to spend time gathering up all of the documents they need for the consideration and approval process. Many of these documents are organizational from the complex itself including:

Covenants and restrictions

HOA bylaws and budgets

Land plat or survey

Minutes from two homeowner’s association meetings

Current financial statements

They will also need to include a letter from an attorney that demonstrates that the complex meets all of the VA’s stringent requirements.

One of the primary factors the VA will be looking for is restrictions that can limit the resale of the property. For example, they will have a difficult time approving a community that has rules to prevent a foreclosure or resale without HOA approval. These can make selling the home burdensome for veterans later on down the road, so it helps for them to clarify the expectations of the complex in advance.

Another major consideration is condos that are located in retirement communities for individuals over the age of 55. It isn’t a given that these types of complexes will receive a denial, but it does require a little more research from the VA and your lender. In this situation, they will be searching for proof that the complex complies with fair housing and lending laws. In short, it comes down to the fact that they do not want to limit the resale of the property in the future.

Timelines

Proving that your desired complex meets all of the VA loan condo requirements can be a time-consuming process. If you are in a hurry to purchase a new home and move in, attempting to purchase a not-yet-approved condo might not be the wisest move. It can be difficult to predict how long it will take for the complex to receive the coveted approval, even if you work with a lender who is experienced with this process.

Sometimes, you might find that the complex and your lender can work together to complete the process smoothly. When a complex is resistant to providing the necessary documentation, the entire approval process can be held up indefinitely. It might still be a slow-moving ordeal even if they are timely with handing over the documents needed to make their complex one of the VA approved condos.

You should be aware that it can take several months for a home to officially meet all of the VA loan condo requirements and receive approval. It takes time for the VA to review all of the documents that are submitted and ensure that you are getting a good deal on a home that can be resold in the future.

Note that your lender cannot order the appraisal until after the approval process is complete. This means that you might be waiting for months to hear that your property is one of the VA approved condos, but it could still fail the VA inspection and derail your financing. The inspection is a crucial part of securing the financing with a VA loan, so it can still take even more time after the final approval is actually issued.

Conclusion

Purchasing a condo is possible with the VA mortgage program, but you will need to ensure that it meets all of the VA loan condo requirements. Obtaining this approval can be a long process that seems challenging and arduous at times. However, it could be an excellent way to purchase the property of your dreams if you have time to spare. Be sure to talk with your real estate professional and your lender to help identify properties that might already fall into the VA approved condos category.

Frequently Asked Questions

Can you finance a condo with a VA loan?

Yes, you can finance condos in a VA-approved project with a VA loan.

Can you use a VA loan to buy a townhouse?

Yes, you can use a VA loan to buy a townhouse in an approved project or complex.

How can I find VA approved condos?

You can search for VA approved condos in their database online here. You might also consider searching for USDA and HUD-approved condos because this could lead to a VA approval as well, provided that the condos were approved before December 2009.

We Specialize in VA Mortgages, Pre Qualify Today – Click Here.

How much can veterans expect to pay for the VA appraisal fees? This inspection is a necessary part of the home buying process for individuals who want to take advantage of the features found in a VA mortgage. Ideally, this ensures that the property meets the minimum standards of safety and sanitation. You should know what this process is going to cost you, especially because it isn’t something you can get out of paying.

How much can veterans expect to pay for the VA appraisal fees? This inspection is a necessary part of the home buying process for individuals who want to take advantage of the features found in a VA mortgage. Ideally, this ensures that the property meets the minimum standards of safety and sanitation. You should know what this process is going to cost you, especially because it isn’t something you can get out of paying.

The VA appraisal fee schedule varies based on your location. It might even vary based on the type of property you are attempting to purchase. For the specific details regarding what the VA appraisal fees in your state are, you can view this map from the Department of Veterans Affairs. By clicking on your state, you can see the fee schedule for your area and your property type.

The VA appraisal fee schedule varies based on your location. It might even vary based on the type of property you are attempting to purchase. For the specific details regarding what the VA appraisal fees in your state are, you can view this map from the Department of Veterans Affairs. By clicking on your state, you can see the fee schedule for your area and your property type. When you purchase a home using a VA mortgage, every eligible property has to pass the VA appraisal and inspection process. The Department of Veterans Affairs has a list of

When you purchase a home using a VA mortgage, every eligible property has to pass the VA appraisal and inspection process. The Department of Veterans Affairs has a list of  Your appraiser has a long list of items they are required to look for during the walkthrough of your property. The roof is simply another item on their list. What exactly is included in their VA loan roof inspection?

Your appraiser has a long list of items they are required to look for during the walkthrough of your property. The roof is simply another item on their list. What exactly is included in their VA loan roof inspection? All homeowners would agree that the roof’s primary function is to keep the elements at bay. You wouldn’t want to purchase a home that already has extensive water stains on the ceiling from an active leak. The ceiling might be bowed from the weight of all the water or it could just be small brown patches that indicate some moisture was recently there. Either way, the appraiser takes this entrance of moisture very seriously.

All homeowners would agree that the roof’s primary function is to keep the elements at bay. You wouldn’t want to purchase a home that already has extensive water stains on the ceiling from an active leak. The ceiling might be bowed from the weight of all the water or it could just be small brown patches that indicate some moisture was recently there. Either way, the appraiser takes this entrance of moisture very seriously. An appraiser wants to see that the roof on your new prospective property is likely to withstand at least two years’ worth of daily wear and tear. That means that most of the shingles should be in place with no leaks on the inside. Any other signs that the roof could be in disrepair are also red flags to an appraiser, including sagging.

An appraiser wants to see that the roof on your new prospective property is likely to withstand at least two years’ worth of daily wear and tear. That means that most of the shingles should be in place with no leaks on the inside. Any other signs that the roof could be in disrepair are also red flags to an appraiser, including sagging. A roof certification is a detailed inspection of the current state of the roof by a licensed specialist. This is different than your home inspector and appraiser. They do not typically have the experience and know-how to issue a thorough VA roof inspection. These experts look at the condition of the roof, including any movement, the soundness of the flashing, and even the gutters and downspouts.

A roof certification is a detailed inspection of the current state of the roof by a licensed specialist. This is different than your home inspector and appraiser. They do not typically have the experience and know-how to issue a thorough VA roof inspection. These experts look at the condition of the roof, including any movement, the soundness of the flashing, and even the gutters and downspouts. Applying for the

Applying for the

You will also receive a couple of

You will also receive a couple of  Before you start entering into the process of purchasing a home with a VA loan, you should be aware of all the buyer requirements.

Before you start entering into the process of purchasing a home with a VA loan, you should be aware of all the buyer requirements.  One of the key questions regarding the buyer requirements is related to the credit score necessary for financing. The good news for many prospective applicants is that there are no minimum credit scores required to receive a VA home loan.

One of the key questions regarding the buyer requirements is related to the credit score necessary for financing. The good news for many prospective applicants is that there are no minimum credit scores required to receive a VA home loan.  The type of properties that qualify for a VA loan is rather extensive, ranging from single-family homes to manufactured homes to condominiums in a VA-approved project. You can even purchase modular homes or build your own home. The only major restrictions are vacant land and co-ops.

The type of properties that qualify for a VA loan is rather extensive, ranging from single-family homes to manufactured homes to condominiums in a VA-approved project. You can even purchase modular homes or build your own home. The only major restrictions are vacant land and co-ops.

The

The

If the home fails the VA appraisal, that doesn’t necessarily mean that all hope is lost. You have a few alternative options to secure the funding you need to make the home your own.

If the home fails the VA appraisal, that doesn’t necessarily mean that all hope is lost. You have a few alternative options to secure the funding you need to make the home your own.  Many prospective home buyers are more interested in purchasing a condo with their

Many prospective home buyers are more interested in purchasing a condo with their  One of the biggest questions facing potential buyers is what VA approved condos actually are. While there are all

One of the biggest questions facing potential buyers is what VA approved condos actually are. While there are all  Condominiums and townhouses can be a great way to receive additional perks to your living situation at no additional cost. Many of these communities provide the same benefits as an apartment complex, including pools or gyms.

Condominiums and townhouses can be a great way to receive additional perks to your living situation at no additional cost. Many of these communities provide the same benefits as an apartment complex, including pools or gyms.