by Leslie Rowberry

Homeowner’s insurance for veterans is the simplest way to protect service members property in the event of a disaster.

Most homeowners will never see a disaster such as a fire or a flood coming their way. Even break-ins are unanticipated events that can rack up thousands of dollars in damage and lost goods.

Finding the right homeowner’s insurance for veterans is an essential way to help mitigate some of the loss you might incur with these disastrous situations.

Finding the right homeowner’s insurance for veterans is an essential way to help mitigate some of the loss you might incur with these disastrous situations.

Your insurance company will help to cover the cost any necessary repairs and replacements based on the type of coverage you keep on the house.

Lenders will require you to keep homeowner’s insurance for veterans on the property you purchase with a VA loan.

This gives them some peace of mind that the property won’t be destroyed before you can finish paying off the loan.

It is a way for them to protect their investment in your house and to ensure that they can recoup the funds on the mortgage if necessary.

Homeowners Insurance for Veterans Coverage Areas

While you might have already heard of homeowners insurance for veterans, some people are still not sure exactly how it protects them.

Insurance companies offer several different policies and types of protection, depending on where you are located.

Insurance companies offer several different policies and types of protection, depending on where you are located.

You will have to use some common sense to consider which types of protection you might need on your home. For example, many insurance policies cover:

- Fire

- Vandalism

- Riots

- Lightening

- Explosions

- Falling Objects

- Freezing

- Weight of snow or ice

- Theft

If you live in the south, you might not have wind or hail coverage because this is not a prominent issue in all parts of the country.

Other individuals will still want to include this in their coverage just in case it ever happened.

Another optional type of coverage is flood insurance. This is generally handled through a separate policy, and it might be required if you live in an area prone to excessive rainwater and flooding.

Not all VA loan homeowner’s insurance will require this separate policy to protect your property.

Types of Coverage

In addition to those scenarios, your home insurance for veterans is going to include four different types of coverage for the damage to your home.

You might have different funds allocated for each of these categories, but most home insurance for veterans includes all four:

You might have different funds allocated for each of these categories, but most home insurance for veterans includes all four:

Structure of the Home:

- You might spend a lot of time considering what a disaster could do to your home, but have you considered what it might do to the structure of your house?

- It might compromise the structural integrity of your foundation, creating a long-lasting issue that will be very expensive to correct.

- Homeowner’s insurance for veterans should help to cover this type of structural damage, as well as any other damage done to the home.

Personal Belongings:

- This type of coverage helps to cover the cost of any damage done to your personal belongings in a covered event.

- Your furniture, clothing, and electronics are all included in this category.

- The insurance company will help you to start over after a disaster, if necessary.

Personal Liability:

- If someone falls on your property or gets bitten by your dog, personal liability helps to protect you.

- You would be considered legally responsible for these events that happen on your property, but homeowner’s insurance for veterans will help to cover the cost of the damage.

Additional Living Expenses:

- Do you need to live somewhere else for a brief period of time while your home is being repaired due to a covered event?

- Homeowner’s insurance can provide you with money to cover the living expenses associated with staying in a motel or renting an apartment for a long-term repair.

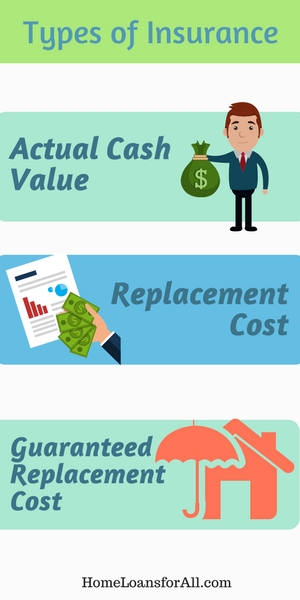

Types of Insurance

Along with the different types of coverage, you also have three different types of homeowner’s insurance to choose from.

This determines to what extent your insurance will help if a covered event occurs on your property.

This determines to what extent your insurance will help if a covered event occurs on your property.

Understanding these terms is very important for your VA loan homeowner’s insurance because it ultimately determines how well your coverage will work.

Actual Cash Value:

- This means that you will receive the amount of money your item is worth minus any depreciation that occurred.

- Whether the insurance company is helping you replace the whole house or just the belongings inside, you are likely to find that actual cash value means you will still be paying for some of your items completely out of pocket.

Replacement Cost:

- In comparison to actual cash value, replacement cost gives you the amount of money it would cost to actually replace your item or home.

- It does factor depreciation into the equation, and it might even give you more than you paid for the item to account for inflation or rising prices on similar items.

Guaranteed Replacement Cost:

- Depending on how badly your home is damaged, you might find that the repair costs actually exceed the policy limits.

- Homeowners who have guaranteed replacement cost insurance don’t need to worry because the insurance company must replace or rebuild the home without factoring in depreciation.

- This guarantee holds true regardless of how much the repair work will actually cost.

What Are the VA Loan Homeowners Insurance Requirements?

All lenders will have a minimum amount of coverage they will expect when you sign up for a VA loan. No matter what company or type of insurance you choose to go with, you will need to have the specified amount of coverage.

Lenders might vary on what they require, but almost all of them will require coverage for at least the loan amount. This protects their interests in the property, no matter what happens.

The other VA loan homeowners insurance requirement is to have a full year of this insurance in place.

Most lenders will want to see the binder that comes toward the beginning of your insurance policy. This is essentially temporary proof of the policy you are signing up for on your home.

This binder should list the deductible, the mortgage company and homeowner as the payee, and the type of coverage you signed up for.

How Can I Save Money When Buying Homeowner’s Insurance?

Fortunately, there are a few ways that you can save on the necessary costs of purchasing homeowner’s insurance for veterans.

With a few of these expert tips, you might be able to save hundreds of dollars per year on your insurance premiums.

Never be afraid to ask the insurance company if there is something you can do to lower your premiums.

The worst thing they can do is tell you no, but you might be able to walk away with substantial savings.

Shopping Around

Always look for insurance at more than one company before you make a final decision.

This gives you a chance to compare rates and types of coverage before you sign on the dotted line.

This gives you a chance to compare rates and types of coverage before you sign on the dotted line.

You can always ask another company to match a lower rate, as long as the coverage is apples to apples.

Raise the Deductible

Raising the deductible is a great way to lower your premiums.

Be prepared that this means you will have a greater out of pocket cost if a disaster ever strikes your property though.

Most homeowners will need to take time to consider what kind of a balance they can strike between a higher deductible and a lower premium before they decide to move forward on this.

Bundling Coverage

Insurance companies are often willing to cut you a discount if you bundle multiple policies all in one place.

For example, you might want to stick with your current provider for auto insurance and life insurance.

When you keep all three policies in one place, it is often cheaper than spreading them out across multiple companies.

Don’t Include the Land

Insuring your land is bound to add some expense to your overall cost of insurance.

You can lower the price of your monthly premiums by insuring only the home and its contents instead of the land.

Stop Smoking

There is a much greater risk of a fire in or around your home if you are an active smoker.

Insurance companies often give lower premiums to individuals who have no smokers in their home.

This is a great time to kick the habit if you are concerned about what your homeowner’s insurance for veterans is likely to cost you.

Group Coverage

You might be able to get a better deal on your homeowner’s insurance through group coverage offered by an employer. Be sure to look into any policies that are available through this avenue.

Stay with Your Current Insurer

Many insurance companies will issue discounts after you have been with them for a long period of time.

By sticking with your current insurer, you might be well on your way to earning a major discount due to your long-term loyalty.

Ask if they will give you a discount for choosing them again with your new home.

Conclusion

Homeowner’s insurance for veterans is necessary if you plan to purchase a home with the VA loan program.

Most lenders will require a minimum amount of coverage to protect their own interests in the property.

With a few of these guidelines, you can be better informed when you select an insurance policy and possibly even save hundreds of dollars on your premium.

Be sure to contact your lender today to see what they require before you start doing your research.

Frequently Asked Questions

What is a homeowner’s insurance binder?

A homeowner’s insurance binder is temporary proof of your coverage. It provides details such as the type of coverage you have, the deductible, and the payee in the event of a major disaster.

What is hazard insurance versus homeowner’s insurance?

Hazard insurance is often considered to be a type of homeowner’s insurance that covers events like fire, hail, theft, vandalism, and similar events. Homeowner’s insurance generally covers these hazards and a wide variety of other events.

Why is homeowner’s insurance required for a VA home loan?

The lender wants to make sure that their investment in the property is protected so they require coverage for at least the loan amount.

Additional Resources

by Leslie Rowberry

Have you always wanted to pull up to a house at the end of the day, proud of the fact that it belongs to you? Bad credit can put your dreams of homeownership on the back burner for years. Fortunately, you can find plenty of home loans for bad credit in Ohio. You have to know where to look for the right deals that can put you well on your way to homeownership.

Have you always wanted to pull up to a house at the end of the day, proud of the fact that it belongs to you? Bad credit can put your dreams of homeownership on the back burner for years. Fortunately, you can find plenty of home loans for bad credit in Ohio. You have to know where to look for the right deals that can put you well on your way to homeownership.

Many people are confused about how their credit score can impede their ability to purchase a home of their own. Lenders often look at these three digits to help them assess how financially responsible you are. Your FICO credit score is based on the information found in your credit report and includes the following categories:

- Payment history

- Amounts owed

- Length of credit history

- Types of credit used

- New credit lines

We Help You Qualify For A Low Credit Loan in Ohio

Fill Out The Form Below To Get Help Today!

All of the small decisions you make with your finances add up to create an overall picture of your financial health. Lenders use this number to determine whether you are likely to repay the loan on time. This is why it can be difficult for borrowers with low credit scores to find lenders willing to issue them a mortgage. The bank is attempting to protect its own interests, so you will need to do a little work on your overall credit first.

How Can I Improve My Credit Score?

The biggest categories for determining your credit score are your payment history and the amounts you own. By addressing these two categories first, you can make a significant improvement in your overall credit score. It does require time to demonstrate that you can rebuild your financial habits and make them healthier again. Remember that you must do these two things consistently in order to see a huge difference in your credit score.

Pay Bills on Time

Payment history is the biggest component of your credit score. So, it’s time to start finding a system that allows you to make payments each and every day. Create a calendar that has all of the due dates and hang it on your refrigerator. Set alarms on your phone that remind you to pay the bills a few days before their actual due date.

Payment history is the biggest component of your credit score. So, it’s time to start finding a system that allows you to make payments each and every day. Create a calendar that has all of the due dates and hang it on your refrigerator. Set alarms on your phone that remind you to pay the bills a few days before their actual due date.

Enrolling in autopay might be the easiest solution if you routinely forget to pay the bills on time. Many companies offer this feature to help make paying your bills easier each month. When you sign up, you give them permission to automatically withdraw the money from your bank account on a specific day each month. You don’t have to think about it and your bills get paid. It’s a win-win situation all the way around.

Pay Down Debt

The other major area where you can gain a quick credit score boost is by paying down some of your debt. Experts recommend using only thirty percent of your available credit lines. Many individuals who have credit cards find that they are well over this recommended amount. Paying off some of your credit card debt so you can be back under this number is a quick and easy way to boost your credit score.

The other major area where you can gain a quick credit score boost is by paying down some of your debt. Experts recommend using only thirty percent of your available credit lines. Many individuals who have credit cards find that they are well over this recommended amount. Paying off some of your credit card debt so you can be back under this number is a quick and easy way to boost your credit score.

Refrain from opening multiple new credit card accounts just to have an excuse to borrow more money. This will still reflect negatively on your credit report and score.

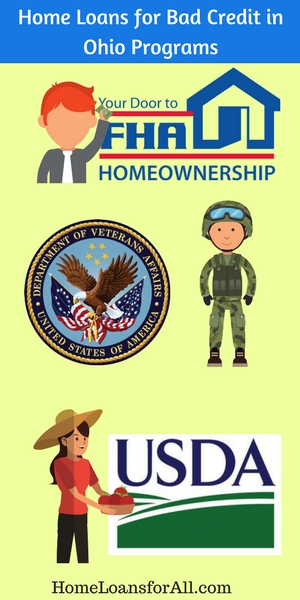

How Can I Find Home Loans for Bad Credit in Ohio?

You already know you have bad credit but still want to pursue homeownership? You need to know where to look for the bad credit home loans in Ohio. There are several federal programs that can help you to purchase a new home in Cleveland, Columbus, Cincinnati, Toledo, or Dayton. No matter where you want to live in the state, there is a perfect option for your home loans for bad credit in Ohio.

FHA Loans

The FHA loan program is a great option for a first time home buyer in Ohio with bad credit. This program is sponsored by the Federal Housing Administration who backs a portion of the mortgage. The government backing on these loans gives lenders more peace of mind to extend financing to borrowers with bad credit or first-time buyers. Not only are they more apt to issue the loan, but they are also able to extend a lot of benefits.

If you are a newbie on our website, you should memorize these logos

Most people searching for home loans for bad credit in Ohio will like the FHA program. It has a very low down payment. Individua and lenient requirements. If you have a credit score of 580 or higher, you only need a 3.5 percent down payment. If you are using the FHA loan as one of the bad credit home loans in Ohio, you might need a greater down payment as a compensating factor. Credit scores between 500 and 579 still qualify for the loan, but you will need a ten percent down payment instead.

VA Loans

Similar to the FHA mortgage, VA loans are sponsored by the Department of Veterans Affairs. They agree to guarantee a portion of each loan for eligible veterans and service members which allows private lenders to issue great terms. You should look for the VA loan program when you are searching for bad credit mortgage lenders in Ohio.

With the VA loan, there is no down payment required and no private mortgage insurance. You will find low-interest rates that accompany these programs as well.

Keep in mind that there are no minimum credit scores required for the VA loan program. The bad credit mortgage lenders in Ohio who offer this program are encouraged to look at your application as a whole before issuing a decision on your financing. A real person is responsible for determining your financial issues and whether any extenuating circumstances contributed to your bad credit. This can be a great way for you to get the help you need to purchase a new home in Cleveland, Columbus, or Cincinnati.

USDA Loan

Do you dream of living in Toledo or Dayton but wish you could live a little further from the city limits? The USDA loan from the United States Department of Agriculture could give you the help you need to purchase a home in a more rural area of the state. This loan program is designed to encourage prospective buyers to help modernize a more rural area. However, only certain properties will be eligible.

If you find a home that qualifies for one of these home loans for bad credit in Ohio, you can apply for this loan. It does not require a down payment and you might be able to add in money for any necessary repairs and renovations at closing.

Much like the VA loan program, there are no minimum credit scores required for the USDA loan. Your application might be subject to manual underwriting if you have a low credit score though. This allows a real person to review your finances and determine whether you are responsible enough to repay the loan. This also means that your financing is highly subjective. If you are denied for one of these bad credit home loans in Ohio, you should try again at a different lender.

How Can I Buy a Home Without a Mortgage?

Have you found that no lenders are eager to issue you the financing you need to purchase a new home? The good news is that you do have two other options if getting a mortgage on your own isn’t a possibility right now. We have two solutions to help you buy a home in top cities like Cleveland, Columbus, Cincinnati, Toledo, and Dayton. The solution suits you even if you can’t qualify for home loans for bad credit in Ohio.

Rent to Own Home in Ohio with Bad Credit

You can still get a rent to own home in Ohio with bad credit, even if you don’t qualify for a mortgage right now. Under this type of purchase, you will find a property listed for sale and sign a lease on it. The owner might ask you for an options fee upfront, which is sort of like a down payment for the new property. A portion of your monthly rent payment will also go toward the principal balance of a future loan. At the end of the lease, you will have the option to purchase the home if you desire.

You can still get a rent to own home in Ohio with bad credit, even if you don’t qualify for a mortgage right now. Under this type of purchase, you will find a property listed for sale and sign a lease on it. The owner might ask you for an options fee upfront, which is sort of like a down payment for the new property. A portion of your monthly rent payment will also go toward the principal balance of a future loan. At the end of the lease, you will have the option to purchase the home if you desire.

During this time, you need to be actively working on your credit score so you can qualify for bad credit home loans in Ohio. You might qualify for more favorable terms and lower interest rates after taking the length of your lease to work on your credit score. Meanwhile, you were able to make a home for yourself while you waited to qualify for home loans for bad credit in Ohio.

This type of getting housing is sometimes risky. Foreclosures sometimes happen. So, you need to be sure that the owner is confident that they want to sell the house eventually.

Get a Cosigner

Please pay your mortgage responsibly, or your friend/relative will have to pay it for you

Are you confident that your financial strife is behind you? You might be able to enlist the help of a friend or family member with excellent credit to help you qualify for a mortgage. When they cosign the loan, the lender also uses their credit score to determine your eligibility for the product. Depending on your own credit score, this could be the boost you need to get your own bad credit home loans in Ohio.

Bear in mind that your cosigner is responsible for your mortgage payments if you make them late or the home moves into foreclosure. Your financial irresponsibility will impact your friend’s credit score directly. Take this into account before you decide to use this method.

What State Programs Are Available in Ohio?

Housing Assistance Grant Program

The Housing Assistance Grant Program from the Ohio Development Services Agency provides some limited down payment assistance programs to low-income and moderate-income families. The grants are issued through the Ohio Housing Trust Fund. It also provides emergency home repairs and handicap accessibility project funding to qualifying homeowners.

Ohio Housing Finance Agency Loan

If you are a first time home buyer in Ohio with bad credit, you may want to look into the Ohio Housing Finance Agency loan. This program provides homeowners in low-income or moderate-income families with financing for their fixed-rate loan, down payment assistance, and a mortgage tax credit. Qualifying families may receive up to five percent in down payment assistance.

You must not have had ownership of a property in the last three years, be an honorably discharged veteran, or purchase a home in a target area to qualify. You must also have a credit score of 640 or higher to qualify for many of their loan options. Homeownership education through HUD is a requirement to receive the loan.

Conclusion

If you want to become a homeowner, there are lots of home loans for bad credit in Ohio to choose from. You should thoroughly investigate what each of your options is before deciding which one is right for you. Most people would agree that it is best to wait until you can raise your credit score. This will give you the chance to qualify for better loans, better terms, and better interest rates. This simple move might delay your dreams of homeownership by a few months or a couple of years. But eventually, it will save you thousands of dollars in the long run.

You still got questions? We still got answers!

Home Loans with Bad Credit in Ohio FAQs

Are there first time home buyer programs in Ohio with bad credit?

Yes, there are first time home buyer programs in Ohio with bad credit. You can apply for FHA loans, VA loans, USDA loans, or the Ohio Housing Finance Agency loan. Contact a lender for more details on these programs and the eligibility requirements.

Where can I find bad credit mortgage lenders in Ohio?

You can find bad credit mortgage lenders in Ohio by searching for lenders that offer the FHA, VA, or USDA loan programs that have no minimum credit score requirements.

Can I purchase a mobile home with home loans for bad credit in Ohio?

Yes, you can purchase a mobile home with bad credit home loans in Ohio.

Additional Resources for Home Loans with Bad Credit in Ohio

by Leslie Rowberry

What are VA Loans in Pennsylvania?

When you’re attempting to purchase a new home in Pennsylvania, you want to ensure that you’re getting the best possible deal. For many individuals and families, Pennsylvania VA loans quickly appear to offer the most favorable terms and benefits. It’s important to fully understand the advantages and the eligibility requirements for applicants interested in VA loans in Pennsylvania.

When you’re attempting to purchase a new home in Pennsylvania, you want to ensure that you’re getting the best possible deal. For many individuals and families, Pennsylvania VA loans quickly appear to offer the most favorable terms and benefits. It’s important to fully understand the advantages and the eligibility requirements for applicants interested in VA loans in Pennsylvania.

These loans are offered through private lenders but are guaranteed in part by the Department of Veterans Affairs. As a result, lenders are more likely to issue loans with better terms to borrowers who may not qualify for conventional mortgage products.

We Specialize in VA Home Loans – Pre Qualify in Pennsylvania Today, click here.

VA Loan Benefits in Pennsylvania

What kind of benefits are truly available with this loan program? For a closer look at the benefits associated with a military mortgage in Pennsylvania, you can see more detailed information below.

No Down Payment

This is perhaps the single largest advantage when it comes to applying for VA loans in Pennsylvania. Traditional mortgage products typically require a twenty percent down payment, which can equate to years’ worth of savings. In comparison, you may be able to purchase a home without any down payment at all.

No Private Mortgage Insurance Premium

When it comes to traditional mortgage products, lenders often require private mortgage insurance when you have a down payment under twenty percent. This insurance premium costs between 0.3 and 1.5 percent of the loan amount annually. These military mortgages in Pennsylvania don’t require private mortgage insurance, which can add up to huge savings on a monthly basis.

No Penalty for Paying Off the Loan Early

Do you want to keep more money in your pocket over the course of your loan? Making extra payments is a great way to reduce the overall cost of your interest rates. A VA loan will allow you to pay off your home early and save on interest costs without any penalty from the lender.

Loan Assistance Available from the VA

If you find yourself struggling to make ends meet, the Department of Veterans Affairs offers help from qualified experts familiar with loan assistance programs to help you avoid foreclosure. Don’t hesitate to reach out if you need help making the monthly payments on your mortgage.

VA Home Loan Eligibility in PA

In order to qualify for a VA loan in Pennsylvania, you will need to determine whether you meet the criteria for a Certificate of Eligibility. Prospective home buyers will need to meet minimum service requirements for active duty in a branch of the armed forces, either during a war or during peacetime. Spouses may also qualify under certain circumstances. You can see the detailed service requirements for a VA loan in Pennsylvania here.

In order to qualify for a VA loan in Pennsylvania, you will need to determine whether you meet the criteria for a Certificate of Eligibility. Prospective home buyers will need to meet minimum service requirements for active duty in a branch of the armed forces, either during a war or during peacetime. Spouses may also qualify under certain circumstances. You can see the detailed service requirements for a VA loan in Pennsylvania here.

Once you can obtain your Certificate of Eligibility, you must select a property that meets the VA loan requirements. There are specific property types that are eligible for these mortgages, including single family homes, condominiums in VA-approved projects, and manufactured homes or lots.

You may be surprised to learn that you can do a number of things with a military mortgage beyond just purchasing a single-family home. Here are some other ways that a military mortgage in

Pennsylvania may be able to help you make homeownership a reality:

Building a new home

Renovating a newly purchased home

Installing energy efficient features or improvements

Refinancing a direct loan to receive a lower interest rate

Refinancing an existing mortgage loan or other indebtedness secured by a lien of record on a home owned and occupied by a veteran as a primary residence

VA Loan Limits by County in Pennsylvania

There is no real maximum dollar amount that a VA loan can have, but most lenders will adhere to specific loan limits set for their county. These are the limits at which prospective buyers can still purchase a home with no down payment. While you can definitely exceed this amount, your lender will likely require you to come up with some type of down payment to cover the difference.

In Pennsylvania, most of the counties will all have the same loan limit. The limit is typically $435,100 based on the average cost of living and the maximums prescribed by Ginnie Mae.

The exception to this loan limit is in Pike County, where the limit is raised to $679,650.

VA Home Loan Pennsylvania Regional Loan Centers

Regional loan centers are a great place to receive additional information regarding a potential military mortgage. You may find yourself filled with tons of questions regarding your eligibility, how the process works, or how to take the first steps. There are eight of these regional loan centers dedicated to helping veterans navigate the waters of homeownership with this mortgage program.

If you are at risk of having your home move into foreclosure, this is also an excellent resource to connect you with loan servicers who may be able to help.

The closest regional loan center to Pennsylvania is actually located in Cleveland.

They are responsible for assisting more than five million individuals in a jurisdiction that includes many of the states in the northeast.

Pennsylvania Home Prices

Do you wonder if you could afford to purchase your own home? It can help to take a look at the median prices of home sales in your area to determine if you can afford it. Real-world numbers can give you a clear glimpse at the current state of the real estate market in your area.

Do you wonder if you could afford to purchase your own home? It can help to take a look at the median prices of home sales in your area to determine if you can afford it. Real-world numbers can give you a clear glimpse at the current state of the real estate market in your area.

The median home price in Pennsylvania is currently on the rise, according to housing market experts.

Over the past few years, it has increased by more than four percent and the trend is likely to continue. Consider the below statistics to determine what you may be able to afford in this state:

Median list price: $189,900

Median sale price: $170,375

Median list price per square foot: $118

Of course, these median prices can change drastically based on the specific area where you may be shopping for a new home. More expensive areas include Philadelphia and Pittsburgh, where you may not get as much house for your money. Both of these cities have seen tremendous growth over the past couple of years.

Currently, the median list price of a home in Philadelphia is almost $195,000 but the median home value is closer to $142,000. Compared to the state as a whole, the square footage price is substantially higher at $143 per square foot.

Pittsburgh is slightly less expensive than Philadelphia, with a median list price coming in right around $190,000. However, the value of homes as a whole is lower than Philadelphia at approximately $129,000. Square foot value is roughly the same as it is across the state at $123 per square foot.

Pennsylvania Regional Benefit Offices for VA Home Loans

For more information regarding the programs available in your area, you can contact one of the local regional benefit offices in Pennsylvania. They can help to answer any questions you may have regarding eligibility for a particular program. These offices may also offer other services that could be beneficial to veterans.

Philadelphia Regional Benefit Office

5000 Wissahickon Avenue

Philadelphia, PA 19144

Pittsburgh Regional Benefit Office

1000 Liberty Avenue

Pittsburgh, PA 15222

Pennsylvania VA Home Loan FAQs

I have bad credit. Can I get a VA loan in Pennsylvania?

Yes, you may still qualify for a VA loan in Pennsylvania even if you have poor credit. There are no minimum credit scores required to be eligible for this loan program. Instead, the federal government is willing to guarantee the loan as long as you can find a lender that will agree to issue a mortgage.

You will need to find a lender that is open to working with individuals who have low credit scores.

Find out how to raise your credit score here.

Can a surviving spouse receive a VA loan in Pennsylvania?

Yes, a surviving spouse can receive a VA loan Pennsylvania when they meet certain requirements. Surviving spouses must remain unmarried until the age of 57 and have been remarried after December 6, 2003. They must also meet the following criteria:

- Must be the spouse of a veteran who died while in service or from a service-connected disability

- Must be the spouse of a service member who is missing in action or a prisoner of war

- Must be the spouse of a totally disabled veteran whose disability may not have been the cause of death

What is the VA loan rate in Pennsylvania?

Unfortunately, there isn’t one standard VA loan rate for all lenders in Pennsylvania. Each lender will set their own unique interest rates based on the state of the economy, competition in the market, credit scores, debt-to-income ratios, and other key factors. Check with your local mortgage company to see what their current rates are for a VA loan Pennsylvania.

Additional Resources for Pennsylvania VA Loans

by Leslie Rowberry

What is a VA Loan?

If you’re considering a VA Home Loan in Texas, you will want to make sure you know all of the details regarding the Texas VA loan limits, benefits, and eligibility criteria.

For those who qualify, a Texas VA Loan often comes with the most favorable loan terms available on today’s market. These loans allow homeowners to celebrate one of the most important milestones while knowing they received substantial savings on the real cost of their home purchase.

For those who qualify, a Texas VA Loan often comes with the most favorable loan terms available on today’s market. These loans allow homeowners to celebrate one of the most important milestones while knowing they received substantial savings on the real cost of their home purchase.

VA loans are obtained through a multitude of private lenders, but they are all backed in part by the Department of Veterans Affairs.

This government-funded support makes lenders more likely to issue loans to applicants who may not qualify for traditional mortgage products. However, this security also enables them to offer more favorable terms to buyers.

We Specialize in Texas VA Home Loans – Click Here to Pre Qualify.

Benefits VA Loans in Texas

These benefits are the key reason why so many individuals and families are applying for a Texas VA loan. Don’t forget to make sure that you understand exactly how this military mortgage program could save you thousands of dollars.

No Down Payment

Many individuals will spend years scraping together the necessary savings for a down payment on a home. In the past, most lenders required a twenty percent down payment. The most significant advantage to the VA loans is that many lenders will not require a down payment at all.

No Private Mortgage Insurance

Private mortgage insurance (often abbreviated PMI) is typically required for homeowners who have a down payment of less than twenty percent. This is often tacked onto the monthly mortgage payment and equates to 0.3 to 1.5 percent of the loan amount annually.

A Texas VA loan allows homeowners to forego making these payments and offers a substantial savings over the duration of the loan.

No Penalty for Paying Off the Loan Early

Even with low VA loan rates, interest can really accumulate over the course of a thirty-year loan. Some homeowners attempt to reduce their out-of-pocket costs by making additional payments to pay off their mortgage early. If you aren’t paying attention, a traditional mortgage may hit you with a penalty for this financially savvy move. Fortunately, VA loans do not have any penalty for early payoff.

Loan Assistance Available from the VA

The ultimate goal is to keep you in your home longer. This is why the Department of Veterans Affairs enlists the help of qualified loan experts to help you find resources and loan assistance programs when you need them. With their aid, you may be able to avoid foreclosure, so don’t hesitate to reach out if you find yourself unable to make ends meet.

Eligibility

Qualifying for a Texas VA loan most often means meeting the criteria for a Certificate of Eligibility. This verifies that you have met the service and time requirements in a branch of the United States armed forces. Depending on the dates, there are many specific criteria regarding service commitments both in peacetime and in wartime. It’s possible that surviving spouses may also qualify for a Texas VA loan.

For more detailed eligibility requirements, you can check the criteria here.

Obtaining your Certificate of Eligibility is the first step in qualifying for a military mortgage. You must also be able to find and decide on a property that is eligible for financing under this program. Fortunately, there are plenty of options to choose from.

Beyond just purchasing a single-family home, prospective buyers can do a number of things with the financing they receive from lenders. They may also purchase a condominium in a VA-approved project or a manufactured home and lot. Your loan can be written to help you build a brand-new home, make renovations to a newly purchased home, or install energy efficient upgrades.

Refinancing options are also available to allow you an opportunity to receive the low VA loan rates in Texas.

VA Loan Limits in Texas by County

How much can you borrow while still taking advantage of the significant benefits associated with a Texas VA loan? This number will ultimately be established based on your credit score, income, debt-to-income ratio, and other key factors. However, there are VA loan limits in Texas.

For most states, the loan limits are broken down by county to accommodate higher costs of living. This is simplified in Texas where all counties have the same VA loan limits this year. In 2018, the VA loan limits in Texas are $453,100.

This essentially means that you cannot borrow more than $453,100 without making a down payment of some kind. It is possible to receive a mortgage that exceeds the VA loan limits in Texas, but it will have a higher upfront cost.

Regional Loan Centers

Regional loan centers are designed to provide veterans and service members with additional information regarding their military mortgage. Representatives are available to help walk you through the eligibility requirements and help you take the first steps on purchasing a home with a Texas VA loan. If you are ever in need of loan assistance, the regional loan center is an excellent resource as well.

There are eight of these centers scattered across the country, but the center assigned to Texas is actually located in Houston. They are also assigned to serve veterans in Mexico, Central and South America, and the Caribbean.

Texas Home Prices

What could you reasonably expect to pay for a new home? Understanding the median prices for homes across Texas can help you to determine affordability and budget your finances accordingly. The median home price has been on the rise across the state, and the current trend seems as though it is likely to continue. For the state as a whole, the median list price of all homes is $269,000 which makes the square foot price come in around $120.

Specific cities may have average home costs that differ from the state as a whole, so we’re also going to take a closer look at three popular cities: San Antonio, Houston, and Dallas. For their median list prices, you can see the statistics below:

- San Antonio: $232,900

- Houston: $324,900

- Dallas: $380,000

As you can see, San Antonio offers more affordable housing in comparison to the two other major cities. Houston and Dallas have square foot prices ($158 and $199 respectively) that exceed the median list prices for the state as a whole.

Click here to find out how Texas Teachers can find assistance in receiving a home loan.

Regional Benefit Offices

You can find more information regarding programs for veterans in your area by contacting one of the regional benefit offices. These offices can help connect you with advantageous services and answer questions regarding eligibility for a particular program.

Houston Regional Benefit Office

6900 Almeda Road

Houston, TX 77030

Waco Regional Benefit Office

701 Clay Avenue

Waco, TX 76799

FAQs

I have bad credit. Can I get a VA loan in Texas?

Yes, you may still qualify for a VA loan in Texas even with a low credit score. There are no minimum credit scores required for this loan program. If you can find a lender willing to work with your credit history, the federal government will still guarantee the loan.

Can a surviving spouse receive a VA loan in Texas?

Under some circumstances, it is possible for a surviving spouse to receive a VA loan in Texas. You must meet some of the following criteria to qualify:

- Must be the spouse of a veteran who died while in service or from a service-connected disability

- Must be the spouse of a service member who is missing in action or a prisoner of war

- Must be the spouse of a totally disabled veteran whose disability may not have been the cause of death

A surviving spouse must remain unmarried until the minimum age of 57. Any new marriage must have also taken place after December 6, 2003, in order to maintain eligibility for VA loans in Texas.

What is the VA loan rate in Texas?

The VA loan rates in Texas will vary based on your unique circumstances and the lender. Mortgage rates constantly fluctuate, but they will often depend on individual factors such as your credit score, debt-to-income ratio, income level, and more. They may also vary due to other factors in the economy. As a result, there are no set VA loan rates in Texas.

Additional Resources for Texans

Home Loans for Nurses in Texas

Home Loans for Teachers in Texas

Home Loans for Single Mothers in Texas

How To Get a Loan With Bad Credit In Texas

Bad Credit Home Loans in Houston, Texas

Bad Credit Home Loans in Fort Worth, Texas

by Leslie Rowberry

The FHA streamline refinance program helps current FHA homeowners lower their rate and payment without most of the traditional refinance documentation. FHA recently lowered its mortgage insurance premiums by 0.50%. Most borrowers can now drop their interest rate and their monthly mortgage insurance with one refinance transaction. To further entice FHA mortgage holders, FHA offers upfront mortgage insurance premium (upfront MIP) refunds. A portion of the premium paid when the original FHA mortgage closed will be applied to the upfront MIP on the new FHA loan.

Get Pre Qualified for An FHA Streamline Refinance Today – Click Here.

FHA Streamline Refinance Advantages

Here are a few of the biggest benefits to the FHA streamline program:

- No appraisal is required

- Underwater homes are eligible

- Very low rates

- No income documentation is required (pay stubs, W2s, etc.)

- You may be entitled to refund of part of your original upfront mortgage insurance

FHA Streamline Refinance Qualifications

The FHA streamline is available to homeowners who currently have an FHA mortgage. In addition, the borrower must have a good payment history. Borrowers must receive a benefit from refinancing. Lenders will approve an FHA loan when the payment will drop by at least 5%.

FHA Streamline Rates

FHA Streamline Rates

Current FHA streamline refinance rates are some of the lowest in history. According to loan software company Ellie Mae, FHA rates are about a quarter percent lower than conventional rates.

Payment History Requirements

To qualify for an FHA streamline loan, you must show a history of making mortgage payments on time. If you have had some late payments, you are not automatically disqualified. You can rebuild your history going forward, and qualify 12 months after your second most recent late payment.

FHA Streamline Waiting Periods

Many homeowners were shocked when FHA announced favorable changes for 2015. Many had just closed their FHA loan at higher MIP levels. The good news is you can use an FHA streamline to lower monthly MIP after as few as six payments.

Closing Costs

Generally you can expect to pay between $1000 and $5000 in FHA streamline closing costs, but this amount could be higher or lower depending on your loan amount and other factors. You may also need to pay a portion of property taxes and insurance at closing.

Lender Credits for Closing Costs

Often, the lender can give you a slightly higher interest rate and use the excess profit from the loan to pay for some or all of your closing costs. If you have equity in your home, it may be possible to obtain an appraisal and wrap the closing costs into the new loan amount.

Appraisals

There are essentially two types of streamline refinances: those with an appraisal and those without. The vast majority of people will opt for the no-appraisal option, simply because the process is quicker and cheaper, and no equity is required.

Maximum FHA Streamline Loan Amount

Quite simply, if you don’t think you have equity in your property, it’s best not to obtain an appraisal.

Do I Need Mortgage Insurance?

On June 11, 2012, FHA reduced its upfront and monthly mortgage insurance (MI) premiums for some borrowers. If your loan was endorsed by FHA on or before May 31, 2009, you are eligible for reduced premiums of .01% upfront MI and .55% monthly MI. There are even mortgage insurance refunds in some cases.

Net Tangible Benefit

The FHA streamline refinance must result in a Net Tangible Benefit (NTB) for the borrower. In other words, the refinance must improve the borrower’s financial position as defined by FHA.

No Longer Required to Close at End of the Month

Up until January 2015, there was a little-known FHA rule stating you had to close your FHA refinance at the end of the month, or pay a double-interest penalty. That is no longer the case.

Minimum Credit Score

FHA does not require a credit report. However, most, if not all lenders will require a credit report. A standard “benchmark” minimum credit score for the FHA streamline program is 640. However, some lenders will allow a score of 620 or even 600. If you are denied, shop around. You might find a lender who approves your application.

Amount of Money Needed to Qualify

You will need to provide 60 days of bank statements showing enough money to cover any out-of-pocket closing costs.

FHA Streamline and Condos

Many condominiums have lost their FHA eligibility over the past few years. However, FHA streamlines are available on condo complexes that were approved at the initial opening of the loan, but have since lost their approval.

The exception is when an appraisal is needed for the FHA streamline. In this case, the condo would need to be FHA approved currently.

What if my home is run down

FHA does not require repairs on a home that is in sub-par condition, as long as there is no appraisal required for the transaction.

Ask your lender about an FHA Streamline Refinance Loan today

Related Articles:

Fannie Mae HomePath Mortgage

10 Ways To Lower Your Mortgage Refinance Rate

FHA Loans vs Conventional Loans